Management Discussion

This document synthesis is waiting to be generated.

Management Discussion

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis provides information that management believes is relevant to an assessment and understanding of our consolidated results of operations and financial condition. You should read this discussion and analysis in conjunction with the consolidated financial statements and notes thereto included elsewhere in this Annual Report on Form 10-K. Certain amounts may not foot or tie to other disclosures due to rounding. Certain information in this discussion and analysis or set forth elsewhere in this Annual Report on Form 10-K contains forward-looking statements that involve numerous risks and uncertainties, including, but not limited to, those described under the sections entitled “Cautionary Note Regarding Forward-Looking Statements” and Part I, Item 1A. “Risk Factors”. We assume no obligation to update any of these forward-looking statements. Actual results may differ materially from those contained in any forward-looking statements.

Business OverviewWe are a member-centric, one-stop shop for financial services that allows members to borrow, save, spend, invest and protect their money. We refer to our customers as “members”, as defined under “Key Business Metrics”. Our mission is to help our members achieve financial independence in order to realize their ambitions. We were founded in 2011 and have developed a suite of financial products that offers the speed, selection, content and convenience that only an integrated digital platform can provide. Everything we do today is geared toward helping our members “Get Your Money Right” and we strive to innovate and build ways for our members to achieve this goal.

In order to help achieve our mission, we offer personal loans, student loans, home loans and related servicing, as well as senior secured loans. We also offer a variety of financial services products, such as SoFi Money checking and savings, SoFi Credit Card, SoFi Invest, and SoFi Relay, that provide more daily interactions with our members, and we offer products and capabilities, such as SoFi At Work, that are designed to appeal to enterprises. We continued to expand our platform capabilities for enterprises through: (i) our acquisition of Galileo in 2020, which provides technology platform services to financial and non-financial institutions and which has allowed us to vertically integrate across more of our financial services, and (ii) the Technisys Merger in the first quarter of 2022, through which we expanded our technology platform services to include a cloud-native, customizable, extensible core technology as well as access to a broader international market. We believe that these expansions will deepen our participation in the entire technology ecosystem powering digital financial services.

See Item 1. “Business—Our Reportable Segments” for a discussion of our segments and their corresponding products. The discussion below focuses on the ways in which our key products and services within each reportable segment generate revenues and/or incur expenses for the Company.

Business Highlights

We achieved strong results for our company for the year ended December 31, 2023, including record total net revenue of $2.1 billion, representing an increase of 35% over total net revenue in 2022. Record revenue at the company level was driven by record net revenue across all three of our business segments. We realized strong momentum in member and product growth and cross-buy adds, reflecting the benefits of our broad product suite and Financial Services Productivity Loop strategy. We added approximately 2.3 million new members during 2023, with over 7.5 million total members as of December 31, 2023, a 44% year over year increase. We also added approximately 3.2 million new products, with over 11.1 million total products as of December 31, 2023, a 41% year over year increase.

Lending segment contribution profit of $823.3 million for the year ended December 31, 2023, at a margin of 60%, increased 24% over 2022, which had a contribution margin of 58%. Total net revenue of $1.4 billion for the year ended December 31, 2023 increased 20% over 2022. Additionally, average net interest margin of 5.88% in 2023 increased 48 basis points compared to 5.40% in 2022. Growth in net interest income was driven by an increase in both average interest-earning assets and average yields, partially offset by an increase in the cost of interest-bearing liabilities. Origination volume increased 34% year over year, primarily driven by demand for personal loans and despite continued macroeconomic headwinds in the student and home loan businesses. Student loans saw some increasing demand in the third quarter of 2023 ahead of the resumption of principal and interest payments on federally-held student loans, and we expect that we may continue to see modest growth in student loan refinancing. Our acquisition of Wyndham in the second quarter of 2023 provided increased capacity and capabilities for our home loans product, which contributed to a notable year over year increase in home loans, and which we expect to continue to provide benefits, while we expect overall home loans growth could be correlated with rate movements in 2024.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Technology Platform segment contribution profit of $94.8 million for the year ended December 31, 2023 increased 24% over 2022, and total net revenue of $352.3 million for the year ended December 31, 2023 increased 12% over 2022. Growth was driven by continued strong organic growth of existing partners and new product adoption, as well as notable contributions from increasingly diversified clients which have launched within the second half of 2023. Margin improvements were driven primarily by Galileo account growth and decreases in directly attributable expenses, as we begin to realize the benefits of earlier investments made to support Technology Platform product development and the integration of Galileo and Technisys. The year over year comparison was also impacted by a partial period of contribution from Technisys in 2022 compared to a full period of contribution in 2023. We continue to make significant strides in our strategy of leveraging our unique product suite to pursue diversified growth and expansion via new products and geographies, in addition to larger, more durable revenue opportunities. We expect growth in segment revenue to continue to accelerate in 2024, as we are well positioned to capture opportunities from traditional financial institutions and nonfinancial categories.

Within Financial Services, contribution loss of $0.3 million for the year ended December 31, 2023 significantly improved compared to a contribution loss of $199.4 million in 2022, and reflected positive contribution profit during the third and fourth quarters of 2023. Total net revenue of $436.5 million for the year ended December 31, 2023 increased 160% over 2022. We achieved continued strong growth in deposits, ending the year with $18.6 billion of deposits as of December 31, 2023, allowing us to maintain diversified sources of funding and driving an increase in net interest income earned on our deposits. In addition, we grew total Financial Services products by 45% year over year. We continue to realize scale in our marketing spend and improvement in operating leverage in the segment. We expect to continue to scale our products through increased brand awareness and network effects, and continue to improve contribution profit in the segment.

The strength of our results underscores our belief that our suite of differentiated products and services provides the foundation for a diversified business that can endure through market cycles as well as exogenous factors. For instance, our access to multiple channels of funding, including deposit and loan warehouse funding, provides an advantage via increased optionality in sourcing liquidity through different environments and periods of capital markets volatility, as well as increases our flexibility to capture additional net interest margin and optimize returns, which typically provides more stable earnings in any macroeconomic environment but is particularly important during times of excess macroeconomic volatility.

During 2023, we continued to have strong deposit contribution from direct deposit members with a high quality median FICO score. We expect that our funding mix will continue to move towards deposit funding, which has a lower borrowing cost of funds than our warehouse and securitization financing model. We also provided our members with access to expanded FDIC insurance coverage through a network of participating banks in our Insured Deposit Program, further enhancing our benefits offering to our members. Our total capital ratio, as calculated under applicable regulatory capital rules, was 15.3% as of December 31, 2023. See Note 21. Regulatory Capital to the Notes to Consolidated Financial Statements for additional information.

Lending Segment

Net interest income, which we define as the difference between the earned interest income and interest expense to finance loans, is a key component of the profitability of our Lending segment. We implemented an FTP framework to attribute net interest income to our business segments based on their usage and/or provision of funding, under which Lending segment net interest income represents the difference between interest income earned on our loans and an FTP charge for the segment’s use of funds to originate loans, which can fluctuate based on changes in interest rates, funding curves, the composition of our balance sheet and the availability of capital. See Note 20. Business Segment and Geographic Information to the Notes to Consolidated Financial Statements for additional information on the FTP framework.

Technology Platform Segment

We earn technology products and solutions fees for providing an integrated platform as a service for financial and non-financial institutions. Many of our Technology Platform segment contracts are multi-year contracts. In certain of our contracts, we provide for a variety of integrated platform services, which vary by client and are either non-cancellable or cancellable with a substantive payment. Pricing structures under these contracts are typically volume-based, or a combination of activity and volume-based, and payment terms are predominantly monthly in arrears. Many of these contracts contain minimum monthly payments, which may result in credits if we do not meet the agreed upon monthly service levels. We also earn subscription and service fees for providing software licenses and associated services, including implementation, maintenance and subsequent development work. We charge a recurring subscription fee for the software license and related maintenance services. Other software-related services are billed on a periodic basis as the services are provided. Certain arrangements for software and related services contain a provision for a fixed upfront payment.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Financial Services Segment

We earn revenues in connection with our Financial Services segment primarily in the following ways:

•Net interest income: Net interest income is a key component of the profitability of our Financial Services segment as it relates primarily to our SoFi Money and credit card products. Net interest income on SoFi Money is based on interest income determined using our FTP framework, net of interest expense based on the interest rate offered to our members on their deposits. Net interest income on credit card is based on the contractual interest included in credit card agreements, net of interest expense as determined using the FTP framework. See Note 20. Business Segment and Geographic Information to the Notes to Consolidated Financial Statements for additional information on the FTP framework.

•Referral fees: Through strategic partnerships, we earn a specified referral fee in connection with referral activity we facilitate through our platform. Referral fees are paid to us by third-party partners that offer services to end users who do not use one of our product offerings, but who were referred to the partners through our platform. We also earn referral fulfillment fees for providing pre-qualified borrower referrals to a third-party partner who separately contracts with a loan originator. Our referral fee is calculated as either a fixed price per successful referral or a percentage of the transaction volume between the enterprise partners and referred consumers.

•Interchange fees: We earn interchange fees from our SoFi-branded debit cards and credit cards. These fees are remitted by merchants and represent a percentage of the underlying transaction value processed through a payment network. We engage a card association and enter into contracts that establish the shared economics of SoFi-branded transaction cards.

•Brokerage fees: We earn brokerage fees primarily from our share lending and payment for order flow arrangements related to our SoFi Invest product, in which we benefit through a negotiated multi-year revenue sharing arrangement, since our members' brokerage activity drives the share lending and payment for order flow volume.

Non-GAAP Financial MeasuresOur management and Board of Directors use adjusted net revenue and adjusted EBITDA, which are non-GAAP financial measures, to evaluate our operating performance, formulate business plans, help better assess our overall liquidity position and make strategic decisions, including those relating to operating expenses and the allocation of internal resources. Accordingly, we believe that these non-GAAP measures provide useful information to investors and others in understanding and evaluating our operating results in the same manner as our management and Board of Directors.

Adjusted Net Revenue

Adjusted net revenue is defined as total net revenue, adjusted to exclude the fair value changes in servicing rights and residual interests classified as debt due to valuation inputs and assumptions changes, which relate only to our Lending segment, as well as gains and losses on extinguishment of debt. We adjust total net revenue to exclude these items, as they are non-cash charges that are not realized during the period, and therefore positive or negative changes do not impact the cash available to fund our operations. This measure helps provide our management with an understanding of the net revenue available to finance our operations and helps management better decide on the proper expenses to authorize for each of our operating segments, to ultimately help achieve target contribution profit margins. Therefore, the measure of adjusted net revenue serves as both the starting point for how we think about the liquidity generated from our operations and also the starting point for our annual financial planning, the latter of which focuses on the cash we expect to generate from our operating segments to help fund the current year’s strategic objectives. Adjusted net revenue has limitations as an analytical tool and should not be considered in isolation from, or as a substitute for, the analysis of other GAAP financial measures, such as total net revenue. The primary limitation of adjusted net revenue is its lack of comparability to other companies that do not utilize this measure or that use a similar measure that is defined in a different manner.

SoFi Technologies, Inc.

TABLE OF CONTENTS

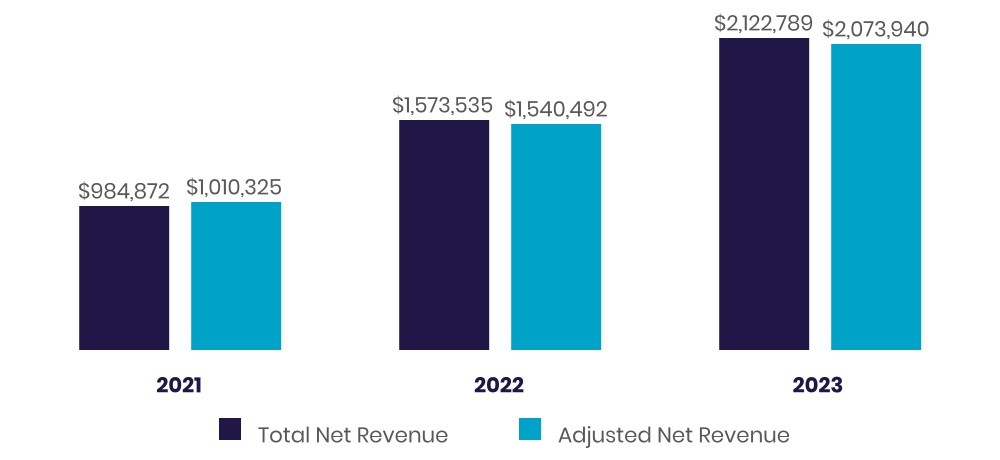

Total Net Revenue and Adjusted Net Revenue

In Thousands

The following table reconciles adjusted net revenue to total net revenue, the most directly comparable GAAP measure:

Year Ended December 31,

($ in thousands) 2023 2022 2021

Total net revenue $2,122,789 $1,573,535 $984,872

Servicing rights – change in valuation inputs or assumptions(1) (34,700) (39,651) 2,651

Residual interests classified as debt – change in valuation inputs or assumptions(2) 425 6,608 22,802

Gain on extinguishment of debt(3) (14,574) — —

Adjusted net revenue $2,073,940 $1,540,492 $1,010,325

(1)Reflects changes in fair value inputs and assumptions on servicing rights, including conditional prepayment, default rates and discount rates. These assumptions are highly sensitive to market interest rate changes and are not indicative of our performance or results of operations. Moreover, these non-cash charges are unrealized during the period and, therefore, have no impact on our cash flows from operations. As such, these positive and negative changes are adjusted out of total net revenue to provide management and financial users with better visibility into the net revenue available to finance our operations and our overall performance.

(2)Reflects changes in fair value inputs and assumptions on residual interests classified as debt, including conditional prepayment, default rates and discount rates. When third parties finance our consolidated securitization VIEs by purchasing residual interests, we receive proceeds at the time of the closing of the securitization and, thereafter, pass along contractual cash flows to the residual interest owner. These residual debt obligations are measured at fair value on a recurring basis, but they have no impact on our initial financing proceeds, our future obligations to the residual interest owner (because future residual interest claims are limited to contractual securitization collateral cash flows), or the general operations of our business. As such, these positive and negative non-cash changes in fair value attributable to assumption changes are adjusted out of total net revenue to provide management and financial users with better visibility into the net revenue available to finance our operations.

(3)Reflects gain on extinguishment of debt. Gains and losses are recognized during the period of extinguishment for the difference between the net carrying amount of debt extinguished and the fair value of equity securities issued. These non-cash charges are not indicative of our core operating performance, and as such are adjusted out of total net revenue to provide management and financial users with better visibility into the net revenue available to finance our operations and our overall performance.

The following table reconciles adjusted net revenue to total net revenue, the most directly comparable GAAP measure, for the quarterly periods presented:

Quarter Ended

($ in thousands) December 31, 2023 September 30, 2023 June 30, 2023 March 31, 2023 December 31, 2022 September 30, 2022 June 30, 2022 March 31, 2022

Total net revenue $615,404 $537,209 $498,018 $472,158 $456,679 $423,985 $362,527 $330,344

Servicing rights – change in valuation inputs or assumptions(1) (6,595) (7,420) (8,601) (12,084) (12,791) (6,182) (9,098) (11,580)

Residual interests classified as debt – change in valuation inputs or assumptions(2) 10 928 (602) 89 (470) 1,453 2,662 2,963

Gain on extinguishment of debt(3) (14,574) — — — — — — —

Adjusted net revenue $594,245 $530,717 $488,815 $460,163 $443,418 $419,256 $356,091 $321,727

SoFi Technologies, Inc.

TABLE OF CONTENTS

(1)See footnote (1) to the table above.

(2)See footnote (2) to the table above.

(3)See footnote (3) to the table above.

The following table reconciles adjusted net revenue for the Lending segment to total net revenue, the most directly comparable GAAP measure for the Lending segment:

Year Ended December 31,

($ in thousands) 2023 2022 2021

Total net revenue – Lending $1,370,621 $1,139,991 $738,323

Servicing rights – change in valuation inputs or assumptions(1) (34,700) (39,651) 2,651

Residual interests classified as debt – change in valuation inputs or assumptions(2) 425 6,608 22,802

Adjusted net revenue – Lending $1,336,346 $1,106,948 $763,776

(1)See footnote (1) to the table above.

(2)See footnote (2) to the table above.

Adjusted EBITDA

Adjusted EBITDA is defined as net income (loss), adjusted to exclude, as applicable: (i) corporate borrowing-based interest expense (our adjusted EBITDA measure is not adjusted for warehouse or securitization-based interest expense, nor deposit interest expense and finance lease liability interest expense, as these are direct operating expenses), (ii) income tax expense (benefit), (iii) depreciation and amortization, (iv) share-based expense (inclusive of equity-based payments to non-employees), (v) restructuring charges (vi) impairment expense (inclusive of goodwill impairment and property, equipment and software abandonments), (vii) transaction-related expenses, (viii) foreign currency impacts related to operations in highly inflationary countries, (ix) fair value changes in warrant liabilities, (x) fair value changes in each of servicing rights and residual interests classified as debt due to valuation assumptions, (xi) gain on extinguishment of debt, and (xii) other charges, as appropriate, that are not expected to recur and are not indicative of our core operating performance. We believe adjusted EBITDA provides a useful measure to investors for period-over-period comparisons of our business, as it removes the effects of certain non-cash items and certain charges that are not indicative of our core operating performance or results of operations. It is also a measure that management relies upon to evaluate cash flows generated from operations, and therefore the extent of additional capital, if any, required to invest in strategic initiatives. Adjusted EBITDA has limitations as an analytical tool and should not be considered in isolation from, or as a substitute for, the analysis of other GAAP financial measures, such as net income (loss). Some of the limitations of adjusted EBITDA include that it does not reflect the impact of working capital requirements or capital expenditures and it is not a universally consistent calculation among companies in our industry, which limits its usefulness as a comparative measure.

Net Loss and Adjusted EBITDA

In Thousands

SoFi Technologies, Inc.

TABLE OF CONTENTS

The following table reconciles adjusted EBITDA to net loss, the most directly comparable GAAP measure:

Year Ended December 31,

($ in thousands) 2023 2022 2021

Net loss $(300,742) $(320,407) $(483,937)

Non-GAAP adjustments:

Interest expense – corporate borrowings(1) 36,833 18,438 10,345

Income tax (benefit) expense(2) (416) 1,686 2,760

Depreciation and amortization(3) 201,416 151,360 101,568

Share-based expense 271,216 305,994 239,371

Restructuring charges(4) 12,749 — —

Impairment expense(5) 248,417 — —

Foreign currency impact of highly inflationary subsidiaries(6) 10,971 — —

Transaction-related expense(7) 142 19,318 27,333

Fair value changes in warrant liabilities(8) — — 107,328

Servicing rights – change in valuation inputs or assumptions(9) (34,700) (39,651) 2,651

Residual interests classified as debt – change in valuation inputs or assumptions(10) 425 6,608 22,802

Gain on extinguishment of debt(11) (14,574) — —

Total adjustments 732,479 463,753 514,158

Adjusted EBITDA $431,737 $143,346 $30,221

(1)Our adjusted EBITDA measure adjusts for corporate borrowing-based interest expense, as these expenses are a function of our capital structure. Corporate borrowing-based interest expense includes interest on our revolving credit facility and the amortization of debt discount and debt issuance costs on our convertible notes, and for 2021, interest on the seller note issued in connection with our acquisition of Galileo. Revolving credit facility interest expense in 2023 and 2022 increased due to higher interest rates relative to the prior years on identical outstanding debt.

(2)Income taxes in 2023 were primarily attributable to income tax benefits from foreign losses in jurisdictions with net deferred tax liabilities related to Technisys, offset by income tax expense associated with the profitability of SoFi Bank in state jurisdictions where separate filings are required, as well as federal taxes where our tax credits and loss carryforwards may be limited. Income taxes in 2022 were primarily attributable to tax expense at SoFi Lending Corp and SoFi Bank due to profitability in state jurisdictions where separate filings are required and recognition of expense from Technisys in certain Latin American countries where separate returns are filed. The expense was partially offset by deferred tax benefits from the amortization of intangible assets acquired in the Technisys Merger. Income taxes in 2021 were primarily attributable to the profitability of SoFi Lending Corp. profitability in state jurisdictions where separate filings are required. See Note 17. Income Taxes to the Notes to Consolidated Financial Statements for additional information.

(3)Depreciation and amortization expense in 2023 increased compared to 2022 primarily in connection with acquisitions and growth in our internally-developed software balance. The increase in 2022 compared to 2021 was primarily in connection with acquisitions and growth in our software balance, partially offset by the acceleration of core banking infrastructure amortization during the 2021 period.

(4)Restructuring charges in 2023 primarily included employee-related wages, benefits and severance associated with a small reduction in headcount in our Technology Platform segment in the first quarter of 2023 and expenses in the fourth quarter of 2023 related to a reduction in headcount across the Company, which do not reflect expected future operating expenses and are not indicative of our core operating performance.

(5)Impairment expense in 2023 includes $247,174 related to goodwill impairment, and $1,243 related to a sublease arrangement, which are not indicative of our core operating performance.

(6)Foreign currency charges reflect the impacts of highly inflationary accounting for our operations in Argentina, which are related to our Technology Platform segment and commenced in the first quarter of 2022 with the Technisys Merger. For the year ended December 31, 2023, all amounts were reflected in the fourth quarter, as inter-quarter amounts were determined to be immaterial. Amounts in 2022 were determined to be immaterial.

(7)Transaction-related expenses in 2023 and 2022 primarily included financial advisory and professional services costs associated with our acquisitions of Wyndham and Technisys, respectively. Transaction-related expenses in 2021 included the special payment to the holders of Series 1 Redeemable Preferred Stock in conjunction with the Business Combination and financial advisory and professional costs associated with our then-pending acquisitions of Golden Pacific and Technisys.

(8)Our adjusted EBITDA measure excludes the non-cash fair value changes in warrants accounted for as liabilities, which were measured at fair value through earnings. The amount in 2021 related to changes in the fair value of Series H warrants issued by Social Finance in connection with certain redeemable preferred stock issuances. We did not measure the Series H warrants at fair value subsequent to May 28, 2021 in conjunction with the Business Combination, as they were reclassified into permanent equity. In addition, in conjunction with the Business Combination, SoFi Technologies assumed certain common stock warrants (“SoFi Technologies warrants”) that were accounted for as liabilities and measured at fair value on a recurring basis. The fair value of the SoFi Technologies warrants was based on the closing price of ticker SOFIW and, therefore, fluctuated based on market activity. The outstanding SoFi Technologies warrants were either exercised during the fourth quarter of 2021 or redeemed on December 6, 2021.

(9)Reflects changes in fair value inputs and assumptions, including market servicing costs, conditional prepayment, default rates and discount rates. This non-cash change is unrealized during the period and, therefore, has no impact on our cash flows from operations. As such, these positive and negative changes in fair value attributable to assumption changes are adjusted out of net loss to provide management and financial users with better visibility into the earnings available to finance our operations.

SoFi Technologies, Inc.

TABLE OF CONTENTS

(10)Reflects changes in fair value inputs and assumptions, including conditional prepayment, default rates and discount rates. When third parties finance our consolidated VIEs through purchasing residual interests, we receive proceeds at the time of the securitization close and, thereafter, pass along contractual cash flows to the residual interest owner. These obligations are measured at fair value on a recurring basis, which has no impact on our initial financing proceeds, our future obligations to the residual interest owner (because future residual interest claims are limited to contractual securitization collateral cash flows), or the general operations of our business. As such, these positive and negative non-cash changes in fair value attributable to assumption changes are adjusted out of net loss to provide management and financial users with better visibility into the earnings available to finance our operations.

(11)Reflects gain on extinguishment of debt. Gains and losses are recognized during the period of extinguishment for the difference between the net carrying amount of debt extinguished and the fair value of equity securities issued. These non-cash charges are not indicative of our core operating performance, and as such are adjusted out of total net revenue to provide management and financial users with better visibility into the net revenue available to finance our operations and our overall performance.

The following table reconciles adjusted EBITDA to net loss, the most directly comparable GAAP measure, for the quarterly periods presented:

Quarter Ended

($ in thousands) December 31, 2023 September 30, 2023 June 30, 2023 March 31, 2023 December 31, 2022 September 30, 2022 June 30, 2022 March 31, 2022

Net loss $47,913 $(266,684) $(47,549) $(34,422) $(40,006) $(74,209) $(95,835) $(110,357)

Non-GAAP adjustments:

Interest expense – corporate borrowings 9,882 9,784 9,167 8,000 7,069 5,270 3,450 2,649

Income tax (benefit) expense 3,245 (244) (1,780) (1,637) 1,057 (242) 119 752

Depreciation and amortization 53,449 52,516 50,130 45,321 42,353 40,253 38,056 30,698

Share-based expense 69,107 62,005 75,878 64,226 70,976 77,855 80,142 77,021

Restructuring charges 7,796 — — 4,953 — — — —

Impairment expense — 247,174 — 1,243 — — — —

Foreign currency impact of highly inflationary subsidiaries 10,971 — — — — — — —

Transaction-related expense — (34) 176 — 1,872 100 808 16,538

Servicing rights – change in valuation inputs or assumptions (6,595) (7,420) (8,601) (12,084) (12,791) (6,182) (9,098) (11,580)

Residual interests classified as debt – change in valuation inputs or assumptions 10 928 (602) 89 (470) 1,453 2,662 2,963

Gain on extinguishment of debt (14,574) — — — — — — —

Total adjustments 133,291 364,709 124,368 110,111 110,066 118,507 116,139 119,041

Adjusted EBITDA $181,204 $98,025 $76,819 $75,689 $70,060 $44,298 $20,304 $8,684

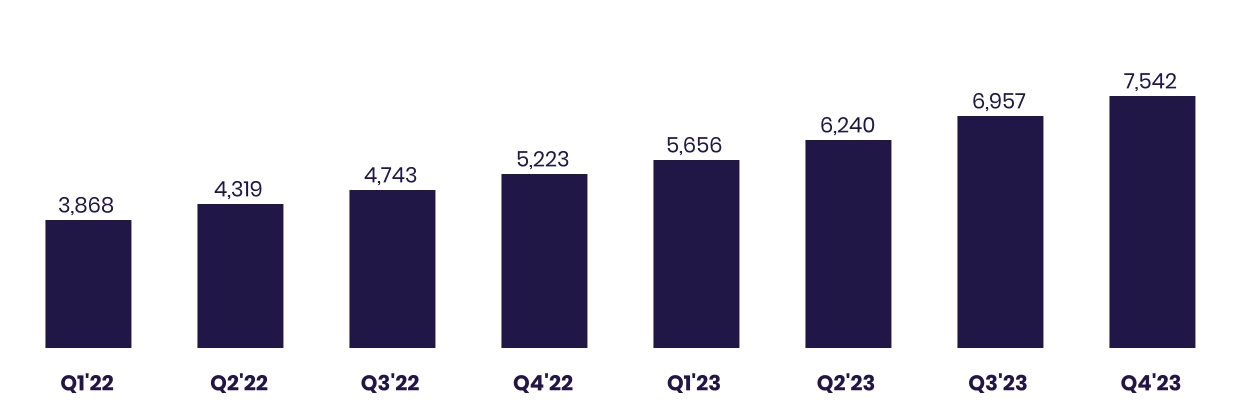

Key Business MetricsThe table below presents the key business metrics that management uses to evaluate our business, measure our performance, identify trends and make strategic decisions:

December 31, 2023 vs. 2022 2022 vs. 2021

2023 2022 2021 # Change % Change # Change % Change

Members 7,541,860 5,222,533 3,460,298 2,319,327 44 % 1,762,235 51 %

Total Products 11,142,476 7,894,636 5,173,197 3,247,840 41 % 2,721,439 53 %

Total Products — Lending segment 1,663,006 1,340,597 1,078,952 322,409 24 % 261,645 24 %

Total Products — Financial Services segment 9,479,470 6,554,039 4,094,245 2,925,431 45 % 2,459,794 60 %

Total Accounts — Technology Platform segment 145,425,391 130,704,351 99,660,657 14,721,040 11 % 31,043,694 31 %

See “Summary Results by Segment” for additional metrics we review at the segment level.

Members

We refer to our customers as “members”. We define a member as someone who has a lending relationship with us through origination and/or ongoing servicing, opened a financial services account, linked an external account to our platform or signed up for our credit score monitoring service. Our members have continuous access to our CFPs, our career advice services, our member events, our content, educational material, news, and our tools and calculators, which are provided at no cost to the member. Additionally, our mobile app and website have a member home feed that is personalized and delivers content to a

SoFi Technologies, Inc.

TABLE OF CONTENTS

member about what they must do that day in their financial life, what they should consider doing that day in their financial life, and what they can do that day in their financial life.

Once someone becomes a member, they are always considered a member unless they violate our terms of service. We adjust our total number of members in the event a member is removed in accordance with our terms of service. This could occur for a variety of reasons—including fraud or pursuant to certain legal processes—and, as our terms of service evolve together with our business practices, product offerings and applicable regulations, our grounds for removing members from our total member count could change. The determination that a member should be removed in accordance with our terms of service is subject to an evaluation process, following the completion, and based on the results, of which, relevant members and their associated products are removed from our total member count in the period in which such evaluation process concludes. However, depending on the length of the evaluation process, that removal may not take place in the same period in which the member was added to our member count or the same period in which the circumstances leading to their removal occurred. For this reason, our total member count may not yet reflect adjustments that may be made once ongoing evaluation processes, if any, conclude.

We view members as an indication not only of the size and a measurement of growth of our business, but also as a measure of the significant value of the data we have collected over time. The data we collect from our members helps us to, among other things: (i) assess loan life performance data on each loan in our ecosystem, which can inform risk-based interest rates that we can offer our members, (ii) understand our members’ spending behavior to identify and suggest other products we offer that may align with the members’ financial needs, and (iii) enhance our opportunities to sell additional products to our members, as our members represent a vital source of marketing opportunities. When we provide additional products to members, it helps improve our unit economics per member, as we save on marketing costs that we would otherwise incur to attract new members. It also increases the lifetime value of an individual member. This in turn enhances our Financial Services Productivity Loop. Member growth is generally an indicator of future revenue, but is not directly correlated with revenues, since not all members who sign up for one of our products fully utilize or continue to use our products, and not all of our products (such as our complimentary product, SoFi Relay) provide direct sources of revenue.

Since our inception through December 31, 2023, we have served approximately 7.5 million members who have used approximately 11.1 million products on the SoFi platform.

Members

In Thousands

Total Products

Total products refers to the aggregate number of lending and financial services products that our members have selected on our platform since our inception through the reporting date, whether or not the members are still registered for such products. Total products is a primary indicator of the size and reach of our Lending and Financial Services segments. Management relies on total products metrics to understand the effectiveness of our member acquisition efforts and to gauge the propensity for members to use more than one product.

In our Lending segment, total products refers to the number of personal loans, student loans and home loans that have been originated through our platform through the reporting date, whether or not such loans have been paid off. If a member has multiple loan products of the same loan product type, such as two personal loans, that is counted as a single product. However,

SoFi Technologies, Inc.

TABLE OF CONTENTS

if a member has multiple loan products across loan product types, such as one personal loan and one home loan, that is counted as two products.

In our Financial Services segment, total products refers to the number of SoFi Money accounts (inclusive of checking and savings accounts held at SoFi Bank and cash management accounts), SoFi Invest accounts, SoFi Credit Card accounts (including accounts with a zero dollar balance at the reporting date), referred loans (which are originated by a third-party partner to which we provide pre-qualified borrower referrals), SoFi At Work accounts and SoFi Relay accounts (with either credit score monitoring enabled or external linked accounts) that have been opened through our platform through the reporting date. Checking and savings accounts are considered one account within our total products metric. Our SoFi Invest service is composed of three products: active investing accounts, robo-advisory accounts and digital assets accounts. Our members can select any one or combination of the types of SoFi Invest products. See Note 1. Organization, Summary of Significant Accounting Policies and New Accounting Standards for additional information on the transfer of the crypto services. If a member has multiple SoFi Invest products of the same account type, such as two active investing accounts, that is counted as a single product. However, if a member has multiple SoFi Invest products across account types, such as one active investing account and one robo-advisory account, those separate account types are considered separate products. In the event a member is removed in accordance with our terms of service, as discussed under “Members” above, the member’s associated products are also removed.

Products

In Thousands

Total lending products were composed of the following:

December 31, 2023 vs. 2022 2022 vs. 2021

Lending Products 2023 2022 2021 Variance % Change Variance % Change

Personal loans 1,113,864 837,462 610,348 276,402 33 % 227,114 37 %

Student loans 519,489 477,132 445,569 42,357 9 % 31,563 7 %

Home loans 29,653 26,003 23,035 3,650 14 % 2,968 13 %

Total lending products 1,663,006 1,340,597 1,078,952 322,409 24 % 261,645 24 %

Total financial services products were composed of the following:

December 31, 2023 vs. 2022 2022 vs. 2021

Financial Services Products 2023 2022 2021 Variance % Change Variance % Change

Money(1) 3,374,310 2,195,402 1,436,955 1,178,908 54 % 758,447 53 %

Invest 2,380,641 2,158,864 1,595,143 221,777 10 % 563,721 35 %

Credit Card 245,385 171,425 91,216 73,960 43 % 80,209 88 %

Referred loans(2) 55,231 40,980 7,659 14,251 35 % 33,321 435 %

Relay 3,336,868 1,921,986 930,181 1,414,882 74 % 991,805 107 %

At Work 87,035 65,382 33,091 21,653 33 % 32,291 98 %

Total financial services products 9,479,470 6,554,039 4,094,245 2,925,431 45 % 2,459,794 60 %

SoFi Technologies, Inc.

TABLE OF CONTENTS

(1) Includes checking and savings accounts held at SoFi Bank, and cash management accounts.

(2) Limited to loans wherein we provide third party fulfillment services.

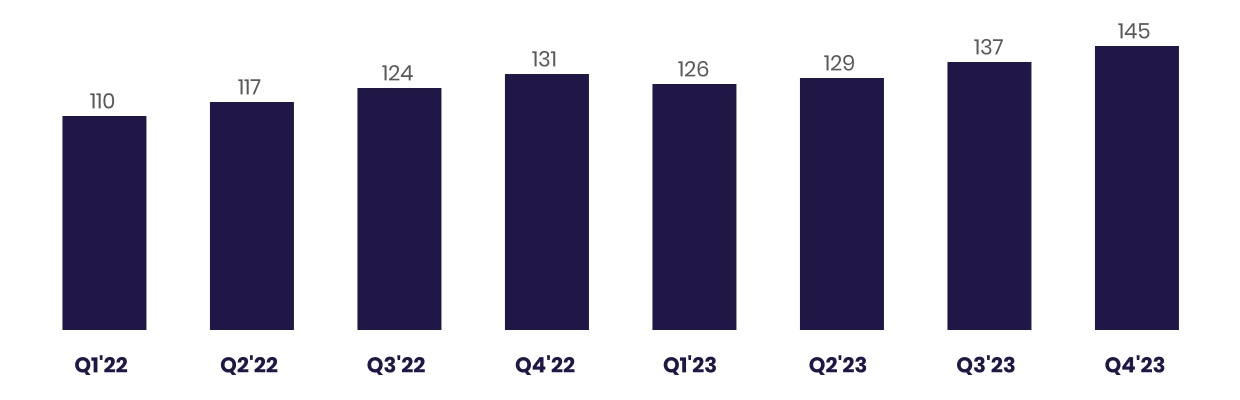

Technology Platform Total Accounts

In our Technology Platform segment, total accounts refers to the number of open accounts at Galileo as of the reporting date. We include intercompany accounts on the Galileo platform as a service in our total accounts metric to better align with the Technology Platform segment revenue reported in Note 20. Business Segment and Geographic Information to the Notes to Consolidated Financial Statements, which includes intercompany revenue. Intercompany revenue is eliminated in consolidation. Total accounts is a primary indicator of the accounts dependent upon our technology platform to use virtual card products, virtual wallets, make peer-to-peer and bank-to-bank transfers, receive early paychecks, separate savings from spending balances, make debit transactions and rely upon real-time authorizations, all of which result in revenues for the Technology Platform segment. We do not measure total accounts for the Technisys products and solutions, as the revenue model is not primarily dependent upon being a fully integrated, stand-ready service.

Technology Platform Accounts(1)(2)

In Millions

(1)We include SoFi accounts on the Galileo platform as a service in Technology Platform total accounts to better align with the presentation of Technology Platform segment total net revenue.

(2)In 2023, Technology Platform total accounts reflects the previously disclosed migration by one of our clients of the majority of its processing volumes to a pure processor. These accounts remained open for administrative purposes through the end of 2022, and were included in our total accounts in such period.

December 31, 2023 vs. 2022 2022 vs. 2021

2023 2022 2021 % Change % Change

Total accounts 145,425,391 130,704,351 99,660,657 11 % 31 %

Key Factors Affecting Operating ResultsOur future operating results and cash flows are dependent upon a number of opportunities, challenges and other factors, including our loan origination volume, financial services products and member activity on our platform, growth in technology platform clients, competition and industry trends, general economic conditions and our ability to optimize our national bank charter.

Origination Volume

Our Lending segment is our largest segment, comprising 65%, 72% and 75% of total net revenue during the years ended December 31, 2023, 2022 and 2021, respectively. We are dependent upon the addition of new members and new activity from existing members within our Lending segment to generate origination volume, which we believe is a contributor to Lending segment net revenue. We believe we have a high-quality loan portfolio, as indicated by our Lending segment weighted average origination FICO score of 749 during the year ended December 31, 2023. See “Industry Trends and General Economic Conditions” for the impact of specific economic factors on origination volume.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Member Growth and Activity

We have invested heavily in our platform and are dependent on continued member growth, as well as our ability to generate additional revenues from our existing members using additional products and services. Member growth and activity is critical to our ability to increase our scale and earn a return on our technology and product investments. Growth in members and member activity will depend heavily on our ability to continue to offer attractive products and services at sustainable costs and our continued member acquisition and marketing efforts.

Product Growth

Our aim is to develop and offer a best-in-class integrated financial services platform with products that meet the broad objectives of our members and the lifecycle of their financial needs. We have invested, and continue to invest, heavily in the development, improvement and marketing of our suite of lending and financial services products and are dependent on continued growth in the number of products selected by our members, as well as our ability to build trust and reliability between our members and our platform to reinforce the effects of the Financial Services Productivity Loop. In order to deliver on our strategy, we aim to foster positive member experiences designed to lead to more product adoption by existing members, leading to enhanced profitability for each additional product by lowering overall member acquisition costs.

Galileo Account Growth

Galileo primarily provides technology platform services to financial and non-financial institutions, which enabled us to diversify our business from a primarily consumer-based business to also serve enterprises that rely upon Galileo’s integrated platform as a service to serve their clients. We are dependent on growth in the number of accounts at Galileo, which is an indication of the amount of users that are dependent upon the technology platform for a variety of products and services, including virtual card products, virtual wallets, peer-to-peer and bank-to-bank transfers, early paychecks and relying on real-time authorizations, all of which generate revenue for Galileo.

SoFi Bank

A key element of our long-term strategy has been to secure a national bank charter. In February 2022, we closed the Bank Merger and began operating Golden Pacific Bank as SoFi Bank. In connection with operating a national bank, we have incurred and expect to continue to incur additional costs primarily associated with headcount, technology infrastructure, governance, compliance and risk management, marketing, and other general and administrative expenses.

See Part I, Item 1. “Company Overview—SoFi Bank” for a discussion of the key expected financial benefits to us of operating a national bank. See Part I, Item 1A. “Risk Factors” for discussion of certain potential risks related to being a bank holding company.

Industry Trends and General Economic Conditions

Our results of operations have historically been relatively resilient to economic downturns but in the future may be impacted by the relative strength of the overall economy and its effect on unemployment, asset markets and consumer spending. As general economic conditions improve or deteriorate, the amount of consumer disposable income tends to fluctuate, which in turn impacts consumer spending levels and the willingness of consumers to take out loans to finance purchases or invest in financial assets. Specific economic factors, such as interest rate levels, changes in monetary and related policies, unemployment rates, market volatility, consumer confidence and changing expectations for inflation and deflation, also influence consumer spending, saving, investing and borrowing patterns.

The Federal Reserve increased the benchmark interest rate throughout 2022 and several times in 2023, largely in response to high inflation, low unemployment and strong consumer demand, while balancing macroeconomic risks, such as increased market volatility. We have continued to see strong demand for our deposits as a result of our competitive interest rate offering and access to expanded FDIC insurance coverage through a network of participating banks in our Insured Deposit Program. However, rising interest rates have unfavorably impacted, and could continue to unfavorably impact, demand for refinancing loan products. Economic and market volatility may continue to occur and could worsen, including if there is additional turmoil in the banking and financial services sectors, which could adversely impact our liquidity, results of operations and financial condition. These market developments have negatively impacted customer confidence in the safety and soundness of certain banks. As a result, although we have not observed a decline in our overall deposits to date, our members may choose to maintain deposits with other financial institutions or spread their deposit funds among multiple financial institutions. In addition, if the Federal Reserve does not effectively curb inflation or interest rates further rise unexpectedly or too quickly or macroeconomic conditions deteriorate or do not improve, it could have a negative impact on the overall economy and result in increased unemployment, which could adversely impact our results of operations. In 2023, we saw a continuation

SoFi Technologies, Inc.

TABLE OF CONTENTS

from 2022 of elevated credit spreads across capital markets and changes in consumer credit. Our increased personal loan annualized charge-off rate year over year was reflective of our expectation of credit metrics to revert over time to more normalized levels, but remains healthy, while our higher credit card annualized charge-off rate was reflective of our maturing portfolio. Negative changes to macroeconomic conditions may result in decreased demand for our products, increased operating costs and negatively impact our results of operations.

Fair Value of Loans

We measure our personal loans, student loans and home loans at fair value. During the year ended December 31, 2023, we transferred home loans out of Level 3 and into Level 2 due to an update to pricing sources utilized by third-party valuation specialists, as part of the integration of Wyndham. Other loans do not trade in an active market with readily observable prices and are classified as Level 3.

Our fair value adjustments on loans impact our consolidated results of operations and include adjustments related to loans originated during the period, loans held at the balance sheet date, as well as gains (losses) on loans sold or repurchased during the period. Fair value adjustments made in each reporting period are impacted by factors such as, among others, interest rates, weighted average coupon, credit spreads, actual and estimated losses, prepayment speeds, duration and previous loan sale execution on similar loans. In determining our fair value assumptions, we incorporate recent data impacting the capital markets, as well as factors specific to us. Changes in these factors, either positive or negative, can have a material impact on our results of operations.

The following table summarizes the significant inputs to the fair value model for personal and student loans:

Personal Loans Student Loans

December 31, September 30, December 31, September 30,

2023 2023 2023 2023

Weighted average coupon rate(1) 13.8 % 13.8 % 5.6 % 5.3 %

Weighted average annual default rate 4.8 4.6 0.6 0.5

Weighted average conditional prepayment rate 23.2 20.3 10.5 10.5

Weighted average discount rate 5.5 6.6 4.3 4.8

(1)Represents the average coupon rate on loans held on balance sheet, weighted by unpaid principal balance outstanding at the balance sheet date.

As of the fourth quarter of 2023 relative to the third quarter of 2023, we observed the following trends:

•The weighted average coupon rates on personal loans and student loans increased by 4 bps and 24 bps, respectively, which reflects rate increases passed on to borrowers related to benchmark interest rates increases during the fourth quarter.

•The weighted average discount rates on personal loans and student loans decreased by 103 bps and 57, respectively, as of December 31, 2023 compared to September 30, 2023. For personal loans, our discount rate assumptions decreased in the fourth quarter due to benchmark rates declining by 90 bps, as well as spreads tightening by 13 bps. For student loans, our discount rate assumptions decreased in the fourth quarter due to benchmark rates declining by 86 bps, as well as spreads widening by 29 bps. Spread changes are indicated by asset-backed security and secondary bond markets.

•Annualized net charge-off rates on personal loans and student loans in the fourth quarter of 2023 were 3.98% and 0.59%, respectively, which remained lower than the assumed weighted average default rates in our fair value model of 4.76% and 0.61%, respectively. Our fair value assumption for annual default rate incorporates fair value markdowns on loans beginning when they are 10 days or more delinquent, with additional markdowns at 30 days, 60 days and 90 days past due. For instance, personal loans are marked down on average 70% when the loans are 30 days past due.

The combination of these and other factors resulted in fair value gains recognized on our personal loans and student loans portfolios during the fourth quarter of 2023.

Student Loan Relief

In June 2023, Congress passed the Fiscal Responsibility Act of 2023 which, among other things, ended the suspension of principal and interest payments on federally-held student loans pursuant to the CARES Act passed in 2020, which became effective 60 days after June 30, 2023, as well as prohibits the Secretary of Education from implementing any extension of any

SoFi Technologies, Inc.

TABLE OF CONTENTS

executive action or rule pursuant thereto. Additionally, in August 2022, President Biden announced relief measures for federal student loan borrowers, including forgiveness of $10,000 of student loans (or up to $20,000 if student loans are Pell Grants) for anyone earning less than $125,000 annually and certain changes to income-driven repayment plans for student loans (the “Biden Forgiveness Program”). Although the U.S. Supreme Court subsequently struck down the Biden Forgiveness Program, President Biden indicated between October 1, 2023 and September 30, 2024, he would allow federal loan borrowers to not be considered delinquent if they miss a payment and that the U.S. Department of Education will not refer borrowers who fail to pay their student loan bills to credit agencies. In addition, on July 14, 2023, President Biden announced that $39 billion in federal student loan debt would be eliminated to remedy mistakes of loan servicers, and other student loan holders will have their loans adjusted. On October 4, 2023, the Biden Administration approved an additional 125,000 borrowers for student loan debt relief, totaling an additional $9 billion in student debt forgiveness.

While we expect we may continue to see an increase in student loan refinancing volume following the end of the federal student loan payment moratorium after August 30, 2023, as borrowers may look to refinance at a lower rate or, given the high interest rate environment, may look to extend the loan term, the timing and impact to our student loan refinancing product will largely depend on expectations regarding the introduction or implementation of additional relief measures, the interest rate environment, how competitive our student loan refinancing products are compared to our competitors and macroeconomic factors.

Key Components of Results of OperationsNet Interest Income

Net interest income primarily reflects the excess of interest income earned on our loans over the interest expense incurred to fund such loans. Net interest income is impacted by loan origination volume, the level of securitization activity, the amount of time we hold loans on our consolidated balance sheet and the volume of member deposits, as well as prevailing interest rates, which impact the rates we receive on our loans and securitization-related investments in bonds and residual interest positions, and the rates we incur from our funding sources including our warehouse facilities, securitization debt and member deposits at SoFi Bank. We also incur interest expense related to our revolving credit facility, as well as on our convertible notes in the form of amortization of debt issuance costs and original issue discount.

Noninterest Income

Noninterest income primarily consists of: (i) revenue recognized from contracts with customers, which primarily relates to our technology products and solutions revenues and has grown due to our recent acquisitions and the growth and expansion of our financial services offerings, (ii) fair value changes in loans while we hold them on our consolidated balance sheet and our securitization activities, inclusive of our hedging activities, (iii) gains on sales of loans transferred into the securitization or whole loan sale channels, (iv) loan origination fees, whereby a borrower may optionally elect to pay origination fees to qualify for a lower annual percentage rate, (v) the income we receive from our loan servicing activities, as well as the assumption of servicing rights from third parties, (vi) gains and losses on non-securitization investments, and (vii) gains and losses on extinguishment of debt.

Noninterest Expense

Noninterest expense primarily relates to the following categories of expenses: (i) technology and product development, (ii) sales and marketing, (iii) cost of operations, and (iv) general and administrative. Certain costs are included within each of these line items, such as compensation and benefits-related expense (inclusive of share-based compensation expense), professional services, depreciation and amortization, and occupancy-related costs. We allocate certain costs to each of these categories based on department-level headcounts. We generally expect these expenses to increase in absolute dollars as our business continues to grow. Noninterest expense also includes the provision for credit losses, which primarily relates to our credit card product, as well as goodwill impairment, related to the Galileo and Technisys reporting units.

Directly Attributable Expenses

As presented within “Summary Results by Segment”, in our determination of the contribution profit (loss) for our reportable segments, we allocate certain expenses that are directly attributable to the segment. Directly attributable expenses primarily include compensation and benefits and sales and marketing, inclusive of member incentives, and vary based on the amount of activity within each segment. Directly attributable expenses also include loan origination and servicing expenses, professional services, product fulfillment and lead generation. Expenses are attributed to the reportable segments using either

SoFi Technologies, Inc.

TABLE OF CONTENTS

direct costs of the segment or labor costs that can be attributed based upon the allocation of employee time for individual products.

Consolidated Results of OperationsThe following table sets forth selected consolidated statements of income data:

Year Ended December 31, 2023 vs. 2022 2022 vs. 2021

($ in thousands) 2023 2022 2021 $ Change % Change $ Change % Change

Net interest income $1,261,740 $584,096 $252,244 $677,644 116 % $331,852 132 %

Total noninterest income 861,049 989,439 732,628 (128,390) (13) % 256,811 35 %

Total net revenue 2,122,789 1,573,535 984,872 549,254 35 % 588,663 60 %

Total noninterest expense 2,423,947 1,892,256 1,466,049 531,691 28 % 426,207 29 %

Loss before income taxes (301,158) (318,721) (481,177) 17,563 (6) % 162,456 (34) %

Income tax benefit (expense) 416 (1,686) (2,760) 2,102 n/m 1,074 (39) %

Net loss $(300,742) $(320,407) $(483,937) $19,665 (6) % $163,530 (34) %

SoFi Technologies, Inc.

TABLE OF CONTENTS

Net Interest Income

The tables below present average balance and interest information for each major category of interest-earning assets and interest-bearing liabilities, along with net interest income and net interest margin.

Average Balances and Net Interest Earnings Analysis

Year Ended December 31,

2023 2022 2021

($ in thousands) Average Balances(1) Interest Income/Expense Average Yield/Rate Average Balances(1) Interest Income/Expense Average Yield/Rate Average Balances(1) Interest Income/Expense Average Yield/Rate

Assets

Interest-earning assets:

Interest-bearing deposits with banks $2,172,013 $91,312 4.20 % $1,122,364 $10,841 0.97 % $706,640 $646 0.09 %

Investment securities 541,590 25,096 4.63 494,005 12,542 2.54 495,444 14,355 2.90

Loans(2) 18,733,812 1,934,659 10.33 9,200,023 749,071 8.14 5,179,729 337,862 6.52

Related party receivables — — — — — — 2,767 211 7.63

Total interest-earning assets 21,447,415 2,051,067 9.56 10,816,392 772,454 7.14 6,384,580 353,074 5.53

Total noninterest-earning assets 3,055,580 2,812,054 1,933,759

Total assets $24,502,995 $13,628,446 $8,318,339

Liabilities, Temporary Equity and Permanent Equity

Interest-bearing liabilities:

Demand deposits $2,214,794 $51,673 2.33 % $1,336,006 $21,814 1.63 % $— $— — %

Savings deposits 8,481,895 359,444 4.24 1,403,750 31,045 2.21 — — —

Time deposits 1,958,002 96,703 4.94 281,633 6,934 2.46 — — —

Total interest-bearing deposits 12,654,691 507,820 4.01 3,021,389 59,793 1.98 — — —

Warehouse facilities 3,142,096 192,987 6.14 2,378,935 71,717 3.01 2,043,085 29,596 1.45

Securitization debt 751,869 36,853 4.90 593,824 22,507 3.79 931,476 35,576 3.82

Other debt(3) 1,638,748 51,526 3.14 1,575,027 30,618 1.94 773,159 27,458 3.55

Total debt 5,532,713 281,366 5.09 4,547,786 124,842 2.75 3,747,720 92,630 2.47

Residual interests classified as debt 12,301 141 1.15 57,510 3,723 6.47 106,990 8,200 7.66

Total interest-bearing liabilities 18,199,705 789,327 4.34 7,626,685 188,358 2.47 3,854,710 100,830 2.62

Total noninterest-bearing liabilities 757,070 657,314 602,994

Total liabilities 18,956,775 8,283,999 4,457,704

Total temporary equity 320,374 320,374 1,637,173

Total permanent equity 5,225,846 5,024,073 2,223,462

Total liabilities, temporary equity and permanent equity $24,502,995 $13,628,446 $8,318,339

Net interest income(4) $1,261,740 $584,096 $252,244

Net interest margin(5) 5.88 % 5.40 % 3.95 %

(1)Average balances were calculated on daily carrying balances for the 2023 period, and on thirteen-month ending carrying balances for the 2022 and 2021 periods, as the daily analysis in the prior periods would have involved undue burden. Both average calculations are representative of our operations.

(2)Interest income on loans measured at amortized cost for the 2022 and 2021 periods includes amortization of deferred loan fees, net of deferred loan costs, which were not material.

(3)Interest expense on other debt primarily includes debt issuance and discount expense, as well as interest expense on the revolving credit facility and seller note, which was repaid in early 2021.

(4)Net interest income is calculated as the excess of total interest income on interest-earning assets over total interest expense on interest-bearing liabilities.

(5)Net interest margin is calculated as net interest income divided by total average interest-earning assets.

2023 vs. 2022. Net interest income increased by $677.6 million, or 116%, during the year ended December 31, 2023 compared to the year ended December 31, 2022, and net interest margin increased by 48 basis points. The increases were primarily driven by higher interest income from (i) personal loans, which was primarily a function of increases in the average balance and origination volume, as well as longer loan holding periods for both personal and student loans, and (ii) interest-

SoFi Technologies, Inc.

TABLE OF CONTENTS

bearing deposits with banks, which reflected our strong liquidity position in a rising interest rate environment. Average interest-earning assets increased by 98%, and average yields increased by 242 basis points.

These increases were partially offset by higher interest expense on deposits attributable to a higher average balance and higher interest rates offered to our members, and higher interest expense on warehouse facilities attributable to a higher average balance and higher interest rates incurred on our facilities, all of which are reflective of the higher interest rate environment year over year.

2022 vs. 2021. Net interest income increased by $331.9 million, or 132%, during the year ended December 31, 2022 compared to the year ended December 31, 2021, primarily driven by higher interest income from non-securitization personal and student loans, which were primarily a function of increases in average balances, higher personal loan origination volume and longer loan holding periods. This increase was partially offset by interest expense on deposits at SoFi Bank during 2022, and lower interest income from consolidated personal and student loan securitizations, which were impacted by decreases in average balances primarily attributable to payment activity and the absence of additions to our consolidated securitization loan balances.

Net interest margin increased by 145 basis points during the year ended December 31, 2022 compared to the year ended December 31, 2021, primarily driven by higher interest-earning assets at higher average yields, particularly related to non-securitization loans, partially offset by higher interest rates paid on warehouse facilities and interest-bearing deposits used to fund our loan originations.

Analysis of Changes in Net Interest Income

The following table presents year-over-year changes in net interest income and the extent to which the variances are attributable to changes in the volume of our interest-earning assets and interest-bearing liabilities or changes in the interest rates related to these assets and liabilities:

2023 vs. 2022 2022 vs. 2021

Increase (Decrease) Due to Change in(1): Increase (Decrease) Due to Change in(1):

($ in thousands) Volume Rate Total Variance Volume Rate Total Variance

Interest income:

Interest-bearing deposits with banks $44,128 $36,343 $80,471 $4,016 $6,179 $10,195

Investment securities 2,205 10,349 12,554 (37) (1,776) (1,813)

Loans 984,564 201,024 1,185,588 327,335 83,874 411,209

Related party receivables — — — — (211) (211)

Total interest income $1,030,897 $247,716 $1,278,613 $331,314 $88,066 $419,380

Interest expense:

Interest-bearing deposits $386,575 $61,452 $448,027 $59,793 $— $59,793

Debt 50,088 106,436 156,524 21,963 10,249 32,212

Residual interests classified as debt (519) (3,063) (3,582) (3,203) (1,274) (4,477)

Total interest expense $436,144 $164,825 $600,969 $78,553 $8,975 $87,528

Net interest income $594,753 $82,891 $677,644 $252,761 $79,091 $331,852

(1)We calculate the change in interest income and interest expense separately for each item. Volume and rate changes have been allocated on a consistent basis using the respective percentage changes in average balances and average rates.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Loan Maturity Schedule

The following table presents the maturities of our loan portfolio, as well as the separate presentation of the total amount of loans in each loan category that are due after one year that have variable rates and fixed rates:

As of December 31, 2023(1)

($ in thousands) Within 1 year After 1 year through 5 years After 5 years through 15 years After 15 years Total

Loan Portfolio:

Personal loans $229,827 $11,758,548 $2,510,254 $— $14,498,629

Student loans 10,153 988,168 3,984,745 1,462,520 6,445,586

Home loans — — — 67,406 67,406

Senior secured loans — 445,733 — — 445,733

Credit card(2) 319,694 — — — 319,694

Commercial and consumer banking 1,565 2,447 12,709 102,242 118,963

Total loans $561,239 $13,194,896 $6,507,708 $1,632,168 $21,896,011

Loans with variable rates:

Personal loans $2,035 $— $— $2,035

Student loans 18,906 80,526 9,769 109,201

Commercial and consumer banking 679 5,532 97,070 103,281

Total loans $21,620 $86,058 $106,839 $214,517

Loans with fixed rates:

Personal loans $11,756,513 $2,510,254 $— $14,266,767

Student loans 969,262 3,904,219 1,452,751 6,326,232

Home loans — — 67,406 67,406

Senior secured loans 445,733 — — 445,733

Commercial and consumer banking 1,768 7,177 5,172 14,117

Total loans $13,173,276 $6,421,650 $1,525,329 $21,120,255

(1)Maturities presented are based upon the contractual terms of the loans. Amounts represent unpaid principal balance of loans outstanding at period end.

(2)Due to the revolving nature of credit cards, we report all of our credit card balances as due within one year.

Noninterest Income and Net Revenue

The following table presents the components of our total noninterest income, as well as total net revenue:

Year Ended December 31, 2023 vs. 2022 2022 vs. 2021

($ in thousands) 2023 2022 2021 $ Change % Change $ Change % Change

Loan origination, sales, and securitizations $371,812 $565,372 $482,764 $(193,560) (34) % $82,608 17 %

Servicing 37,328 43,547 (2,281) (6,219) (14) 45,828 n/m

Technology products and solutions 323,972 304,901 191,847 19,071 6 113,054 59

Other 127,937 75,619 60,298 52,318 69 15,321 25

Total noninterest income $861,049 $989,439 $732,628 $(128,390) (13) $256,811 35

Total net revenue $2,122,789 $1,573,535 $984,872 $549,254 35 % $588,663 60 %

2023 vs. 2022. Total noninterest income decreased by $128.4 million, or 13%, for the year ended December 31, 2023 compared to the year ended December 31, 2022, which was primarily attributable to: (i) higher personal loan write-offs in 2023, (ii) higher origination fees primarily related to a new product feature offered on personal loans, whereby a borrower may optionally elect to pay origination fees to qualify for a lower annual percentage rate, (iii) the net effect of higher income related to in period originations, loan sale execution and fair value adjustments on loans and securitization loans, which were primarily impacted by higher personal loan origination volume, lower student loan prepayment assumptions, and an increase in securitization loan fair market values primarily associated with a consolidated securitization transaction in the first quarter of 2023, partially offset by losses in 2023 compared to gains in 2022 on loan hedging and risk retention hedge activities due to smaller increases in interest rates during the 2023 period, (iv) growth in technology products and solutions fees largely driven

SoFi Technologies, Inc.

TABLE OF CONTENTS

by revenue contribution from Technisys for the full period in 2023, (v) increased interchange revenue, and (vi) gain on extinguishment of debt during 2023.

2022 vs. 2021. Total noninterest income increased by $256.8 million, or 35%, for the year ended December 31, 2022 compared to the year ended December 31, 2021, primarily driven by loan hedging activities due to higher interest rates in 2022, partially offset by lower income related to in period originations, loan sale execution and fair value adjustments on loans, as well as higher loan write offs. The increase was also attributable to growth in technology products and solutions fees driven by account growth and increased activity among our existing integrated technology solutions clients combined with revenue contribution from the Technisys Merger in 2022.

Noninterest Expense

The following table presents the components of our total noninterest expense:

Year Ended December 31, 2023 vs. 2022 2022 vs. 2021

($ in thousands) 2023 2022 2021 $ Change % Change $ Change % Change

Technology and product development $511,419 $405,257 $276,087 $106,162 26 % $129,170 47 %

Sales and marketing 719,400 617,823 426,875 101,577 16 190,948 45

Cost of operations 379,998 313,226 256,980 66,772 21 56,246 22

General and administrative 511,011 501,618 498,534 9,393 2 3,084 1

Goodwill impairment 247,174 — — 247,174 n/m — n/m

Provision for credit losses 54,945 54,332 7,573 613 1 46,759 617

Total noninterest expense $2,423,947 $1,892,256 $1,466,049 $531,691 28 % $426,207 29 %

2023 vs. 2022. Total noninterest expense increased by $531.7 million, or 28%, for the year ended December 31, 2023 compared to the year ended December 31, 2022, primarily driven by: (i) goodwill impairment expense related to the Galileo and Technisys reporting units, further discussed within “Critical Accounting Policies and Estimates—Goodwill”, (ii) higher employee compensation and benefits, which was attributable to increases in headcount and salary and the inclusion of Technisys for the full 2023 period compared to a partial period in 2022, related to support of our growth and impacts of the inflationary environment, as well as restructuring charges during the first and fourth quarters of 2023 and partially offset by decreases in share-based compensation expense, (iii) increases in advertising and marketing expenditures, utilization of lead generation channels and direct member incentives, (iv) increased amortization of purchased and internally-developed software, and in tools and subscriptions costs, reflective of continued investments in technology, (v) an increase in product fulfillment costs, which included debit card fulfillment services, primarily related to our SoFi Money product, as well as payment processing network association fees associated with increased activity on our technology platform, and (vi) increases in amortization of intangible assets primarily due to acquired intangible assets in the Technisys Merger and Wyndham acquisition. These increases were partially offset by the absence of transaction expenses that were incurred in the 2022 period related to our acquisition of Technisys.

2022 vs. 2021. Total noninterest expense increased by $426.2 million, or 29%, for the year ended December 31, 2022 compared to the year ended December 31, 2021, primarily driven by: (i) higher employee compensation and benefits (inclusive of an increase in share-based compensation expense), a portion of which was attributable to the Technisys Merger and the remainder of which was related to increased personnel to support our growth in 2022, (ii) increases in advertising expenditures and utilization of lead generation channels, (iii) an increase in the provision for credit losses, which reflected higher average credit card balances combined with elevated credit card loss rates during 2022, (iv) an increase in amortization of intangible assets due to acquired intangible assets in the Technisys Merger, and (v) an increase in purchased and internally-developed software amortization, reflective of continued investments in technology.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Provision for Credit Losses

Analysis of Allowance for Credit Losses

Allowance for Credit Losses Ratios

The following table presents the ratio of allowance for credit losses to total loans outstanding that are measured at amortized cost:

December 31,

($ in thousands) 2023 2022

Allowance for credit losses to total loans outstanding

Allowance for credit losses $54,695 $40,788

Total loans held for investment, at amortized cost outstanding(1) $884,390 $344,106

Ratio(2) 6.18 % 11.85 %

(1)Total loans outstanding excludes accrued interest.

(2)The decrease in the ratio was primarily attributable to senior secured loans, for which we did not recognize an allowance for credit losses, partially offset by credit cards, which was primarily reflective of an increase in the average balance combined with elevated loss rates.

We omitted the credit ratios associated with nonaccrual loans, as the balance of nonaccrual loans was immaterial.

Allocation of Allowance for Credit Losses

The following table presents the allocation of the allowance for credit losses and the percentage of loans outstanding by category to total loans outstanding that are measured at amortized cost:

December 31, 2023 December 31, 2022

($ in thousands) Allowance for credit losses Percent of loans to total loans(1) Allowance for credit losses Percent of loans to total loans(1)

Credit card $52,385 36 % $39,110 71 %

Commercial and consumer banking 2,310 13 1,678 29

Senior secured loans(2) — 51 — —

Total $54,695 100 % $40,788 100 %

(1)Loans outstanding balances used in the calculation exclude accrued interest.

(2)For the periods presented, we did not recognize an allowance for credit losses on senior secured loans, as we determined that our expected exposure to credit losses was immaterial.

Analysis of Charge-offs

The following tables present information regarding average loans outstanding, net charge-offs and the annualized ratio of net charge-offs to average loans outstanding:

Year Ended December 31,

2023 2022 2021

($ in thousands) Average Loans(1) Net Charge-offs(2) Ratio Average Loans(1) Net Charge-offs(2) Ratio Average Loans(1) Net Charge-offs(2) Ratio

Personal loans $12,638,807 $432,706 3.42 % $4,767,708 $88,511 1.86 % $1,968,297 $19,398 0.99 %

Student loans 5,641,787 25,048 0.44 4,059,001 12,677 0.31 2,964,404 9,399 0.32

Home loans 78,554 — — 132,663 — — 197,452 — —

Senior secured loans 26,291 — — — — — — — —

Credit card(3) 238,832 40,992 17.16 167,290 20,957 12.53 47,533 2,048 4.31

Commercial and consumer banking 109,541 46 0.04 73,361 7 0.01 2,043 — —

Total loans $18,733,812 $498,792 2.66 % $9,200,023 $122,152 1.33 % $5,179,729 $30,845 0.60 %

SoFi Technologies, Inc.

TABLE OF CONTENTS

(1)Average balances were calculated on daily carrying balances for the 2023 period, and on thirteen-month ending carrying balances for the 2022 and 2021 periods, as the daily analysis in the prior periods would have involved undue burden. Both average calculations are representative of our operations.

(2)Net charge-offs include both credit- and certain non-credit-related charge-offs.

(3)The increase in the net charge-off rate associated with credit card was primarily related to our maturing portfolio.

2022 vs. 2021. The provision for credit losses increased by $46.8 million, which primarily reflected higher average credit card balances combined with elevated credit card loss rates during 2022.

Income Taxes