Business Description

This document synthesis is waiting to be generated.

Business Description

Item 1. Business

Company Overview

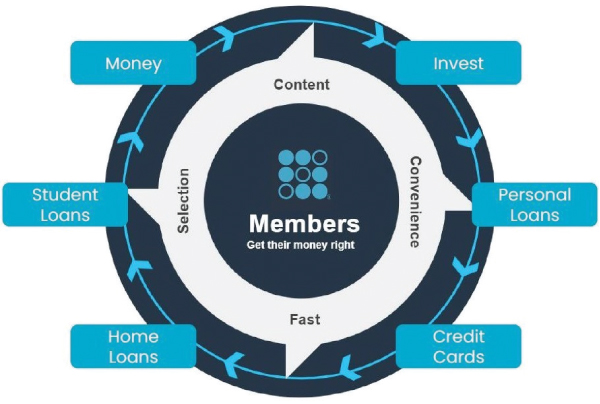

We are a member-centric, one-stop shop for financial services that, through our Lending and Financial Services products, allows members to borrow, save, spend, invest and protect their money. We refer to our customers as “members”. Our mission is to help our members achieve financial independence in order to realize their ambitions. To us, financial independence does not mean being wealthy, but rather represents the ability of our members to have the financial means to achieve their personal objectives at each stage of life, such as owning a home, having a family, or having a career of their choice — more simply stated, to have enough money to do what they want. We were founded in 2011 and have developed a suite of financial products that offers the speed, selection, content and convenience that only an integrated digital platform can provide. In order for us to achieve our mission, we have to help people get their money right, which means providing them with the ability to borrow better, save better, spend better, invest better and protect better. Everything we do today is geared toward helping our members “Get Your Money Right” and we strive to innovate and build ways for our members to achieve this goal.

We have built a social area within our digital native application, which we refer to as the member home feed. The member home feed is personalized and delivers content to a member about what they must do that day in their financial life, what they should consider doing that day in their financial life, and what they can do that day in their financial life. Through the member home feed, there are significant opportunities to build frequent engagement and, to date, the member home feed has been an important driver of new product adoption. The member home feed is an important part of our strategy and our ability to use data as a competitive advantage.

To complement these products and services, we believe in establishing partnerships with other enterprises to leverage our existing capabilities to reach a broader market and in building vertically-integrated technology platforms designed to manage and deliver our suite of products and technology solutions to our members and clients in a low-cost and differentiated manner.

Our three reportable segments and their primary product offerings as of December 31, 2022 were as follows:

(1)Composed of in-school loans and student loan refinancing.

(2)Our SoFi Invest service is composed of three products: active investing accounts, robo-advisory accounts and digital assets accounts. SoFi Invest also includes our brokerage accounts through 8 Limited in Hong Kong.

Recent Acquisitions

In February 2022, we closed the Bank Merger, after which we became a bank holding company and Golden Pacific began operating as SoFi Bank. We believe operating a national bank allows us to provide members and prospective members broader and more competitive options across their financial services needs and lowers our cost of asset-backed financing relative to alternative sources of funding (by utilizing deposits held at SoFi Bank to fund our loans). We also believe that operating as a national bank enables us to offer lower interest rates on loans to members as well as offer higher interest rates on deposit accounts. See “SoFi Bank” herein for additional information on the Bank Merger.

SoFi Technologies, Inc.

TABLE OF CONTENTS

In March 2022, we closed the Technisys Merger, which added a cloud-native digital and core banking platform with an existing footprint of clients into our technology platform offerings. We believe that the combination of the Technisys core banking platform with our existing technology platform offerings provides an end-to-end vertically integrated technology stack, which we expect will meet the expanding needs of our existing clients and attract new clients.

See Note 2 to the Notes to Consolidated Financial Statements for additional information on our business combinations.

Members

We have created an innovative financial services platform designed to offer best-in-class products to meet the broad objectives of our members and the lifecycle of their financial needs. Our platform offers our members (as defined under Part II, Item 7. “Key Business Metrics”) a suite of financial products and services, enabling them to borrow, save, spend, invest and protect their finances across one integrated platform. Our aim is to create a best-in-class, integrated financial services platform that will generate a virtuous cycle whereby positive member experiences will lead to new product adoption by existing members and enhanced profitability for each additional product by lowering overall member acquisition costs and increasing the lifetime value of our members. We refer to this virtuous cycle as our “Financial Services Productivity Loop”, which is further discussed below.

Enterprises

In addition to benefiting our members, our products and capabilities are also designed to appeal to enterprises, such as financial services institutions that subscribe to our enterprise services and have become interconnected with the SoFi platform. We have continued to expand our platform capabilities for enterprises through our acquisition of Galileo in 2020, which provides technology platform services to financial and non-financial institutions and which has allowed us to vertically integrate across more of our financial services, and the Technisys Merger in the first quarter of 2022, through which we added a cloud-native digital and core banking platform into our technology platform offerings and expanded our technology platform services to a broader international market. We believe that these expansions will deepen our participation in the entire technology ecosystem powering digital financial services, allowing us to not only reduce costs to operate our member-centric business, but also deliver increasing value to our enterprise customers. While our enterprises are not considered members, they are important contributors to the growth of the SoFi platform, and also have their own constituents who might benefit from our products in the future.

SoFi Bank

In February 2022, we closed the Bank Merger, pursuant to which we acquired all of the outstanding equity interests in Golden Pacific Bancorp, Inc. and its wholly-owned subsidiary, Golden Pacific Bank, a national bank. Upon closing the Bank Merger, we became a bank holding company and Golden Pacific began operating as SoFi Bank. Golden Pacific’s community bank business continues to operate as a division of SoFi Bank.

As a bank holding company, we offer SoFi Checking and Savings accounts through SoFi Bank. We are originating all new loan applications within SoFi Bank and transferred SoFi Credit Card and the majority of other lending products to SoFi Bank. We intend to continue to explore other products for SoFi Bank over time. The key current and expected financial benefits to us of operating a national bank include: (i) lowering our cost to fund loans, as we can utilize deposits held at SoFi Bank to fund loans, which have a lower borrowing cost of funds than our warehouse and securitization financing model, (ii) increasing our flexibility to hold loans on our balance sheet for longer periods, thereby enabling us to earn interest on these loans for a longer period, (iii) supporting origination volume growth by providing an alternative financing option, while also maintaining our warehouse capacity, and (iv) through deposits, providing us with meaningful member data that can allow us to better serve their financial needs. See Part I, Item 1A. “Risk Factors” for a discussion of certain potential risks related to being a bank holding company.

International Operations

While we primarily operate in the United States, we expanded into Hong Kong with our acquisition of 8 Limited (an investment business) in 2020, we gained clients in Canada, Mexico and Colombia with our acquisition of Galileo in 2020, and we further expanded into Latin America with the Technisys Merger in 2022.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Our DifferentiationIn order to build best-in-class offerings, we focus on four differentiators: fast, selection, content and convenience.

(1)Fast — We aspire to be the fastest place for our members to responsibly do anything, whether it’s applying for a loan, getting a funded loan, opening an account, buying or selling a stock, uploading a mobile check, getting access to money, paying a friend, or accessing relevant financial content. Other than certain products acquired and offered through SoFi Bank, our products are all digital and we have a culture of iteration to help drive faster and faster services.

(2)Selection — Given the digital nature of our products, the permutations of features and services that can be made available to our members across their needs to borrow, save, spend, invest and protect are significant. We will continue to iterate, learn and innovate to broaden our selection in the same way we did this year by providing our members with competitive interest rates on checking and savings accounts, options trading, “Pay in 4” (a buy now, pay later product), and SoFi Plus membership benefits.

(3)Content — Our financial education, insights, research content, actionable tools and advice are designed to provide meaningful value for our members. Our carefully-crafted and personalized content is offered through our member home feed and is designed to help our members get their money right. We strive to provide digestible financial education, meaningful answers, salient information, advice, credit scores, financial calculators, investment research and financial news that enhance member loyalty and increase the likelihood that members will use additional SoFi products in the future.

(4)Convenience — We hold ourselves accountable and aim to provide the most convenient member experience possible in terms of ease of use, ubiquity, functionality, simplicity and responsive customer service. Our long-term goal is to provide the most convenient 24x7 service and dispel the historical construct of financial service availability based on 9-5 Monday through Friday.

Each product we offer is delivered in a member-centric way and is built and enhanced with these differentiators in mind. We believe that our member-centric, one-stop shop for financial services serves as a competitive differentiator for us relative to other financial services providers.

We offer our members a full suite of financial products and services all in one common mobile platform. To complement these products and services, we believe in building vertically-integrated technology platforms designed to manage and deliver the suite of solutions to our members in a low-cost and differentiated manner.

The Financial Services Productivity LoopWe believe that developing a relationship with our members and gaining their trust is central to our success as a financial services platform. Moreover, we believe that some of the current frictions faced by other financial institutions are caused by a disjointed and non-seamless product experience, a lack of digital acquisition, subpar mobile web products instead of digital native apps and incomplete product offerings to meet a customer’s holistic financial needs. Through our mobile technology and continuous effort to improve our financial services products, we are seeking to build a financial services platform that members can access for all of their financial services needs.

Our strategy, which is rooted in what we refer to as our “Financial Services Productivity Loop”, is centered around building trust and a lifetime relationship with our members, which we believe will help build a sustainable competitive advantage.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Financial Services Productivity Loop

In order to deliver on our strategy, we must develop best-in-class unit economics and best-in-class products that build trust and reliability between our members and our platform. Our acquisition of SoFi Bank was also an important step in continuing to build best-in-class unit economics and best-in-class products, as it has enabled us to offer additional products and achieve lower cost of funding. When we do this on a member’s first product, and they later consider using an additional product, we believe they are more likely to start with our platform and we have a higher chance that they will select one of our products to meet their other financial needs. This results in delivering more revenue per member with no second member acquisition costs, resulting in higher lifetime value per member. This also reinforces the benefits of our platform, which simplifies the entire financial ecosystem for our members, helping them get their money right. We are able to use the increased profits to further improve member benefits and product experience.

In addition to realizing the benefits of more of our members adopting multiple SoFi products, the Financial Services Productivity Loop strategy delivers operating and technology efficiencies to deliver better unit economics on a per product basis. One of the success factors of our lending business is that it is vertically integrated across our technology stack, risk protocols and operations processes.

Our Reportable SegmentsWe conduct our business through three reportable segments: Lending, Technology Platform and Financial Services. Below is a discussion of our segments and their primary products.

Lending Segment

We offer personal loans, student loans and home loans and related servicing. We believe that our market opportunity within each of these lending channels is significant. Our lending process primarily leverages an in-application, digital borrowing experience, which we believe serves as a competitive advantage as digital lending becomes increasingly ubiquitous. Furthermore, our platform supports the full transaction lifecycle, including credit application, underwriting, approval, funding and servicing. Through data derived at loan origination and throughout the servicing process, SoFi has life-of-loan performance data on each loan in our ecosystem that we originate and on which we retain servicing, which provides a meaningful data asset. Net interest income, which we define as the difference between the earned interest income and interest expense to finance loans, is a key component of the profitability of our Lending segment.

Personal Loans. We originate personal loans to help our members with a variety of financial needs, such as debt consolidation, home improvement projects, family planning, travel and weddings, to name a few. We offer fixed rate loans with flexible repayment terms, including unemployment protection. We generally offer loan sizes of $5,000 to $100,000, subject to legal and/or licensing requirements, with terms generally ranging from 2 to 7 years. We regularly update the annual percentage rates offered on our personal loans.

Student Loans. We operate in the student loan refinance space, with a focus on prime and super-prime school loans, as well as the “in-school” lending space, which allows members to borrow funds while they attend school. We offer flexible loan sizes and repayment options, competitive rates and, in most cases, the ability to lock in an interest rate for funding at a later

SoFi Technologies, Inc.

TABLE OF CONTENTS

time. Within student loan refinancing, we generally offer loan sizes of $5,000 or higher, subject to legal and/or licensing requirements, with terms generally ranging from 5 to 20 years. Within in-school loans, we generally offer loan sizes of $1,000 or higher, subject to legal and/or licensing requirements, with terms generally ranging from 5 to 15 years. We regularly update the annual percentage rates offered on our fixed and variable-rate student loans.

Home Loans. We offer agency and non-agency loans for members purchasing a home or refinancing an existing mortgage. For our home loan products, we offer competitive rates, flexible down payment options for as little as 3%, a close on time guarantee, and educational tools and calculators. We generally offer loan sizes of $100,000 to $726,200 for one-unit properties in conforming normal cost areas (with exceptions for loan sizes less than $100,000 considered on a case-by-case basis), up to $1,089,300 for conforming high cost areas (Government-Sponsored Enterprises, or “GSEs”, eligible loans above the normal conforming limit, which is determined by county) and up to $3,000,000 for jumbo loans (loans in the jumbo loan program). Our fixed rate home loans generally have terms of 10, 15, 20 or 30 years. We recently began offering an adjustable rate mortgage product for conforming and jumbo loans, with a fixed rate for 5, 7 or 10 years followed by rate adjustments every six months for the remainder of the 30-year term. We regularly update the annual percentage rates offered on our home loans.

Lending Model

Although our lending business remains primarily a gain-on-sale model, whereby we seek to originate loans, recognize a gain from these loans and sell them into either our whole loan or securitization channels, operating SoFi Bank has also provided us with more flexibility to hold loans on our balance sheet for longer periods, thereby enabling us to earn interest on these loans for a longer period and to be selective in our sales arrangements. We sell our whole loans primarily to large financial institutions, such as bank holding companies. In securitization transactions that do not qualify for sale accounting, the related assets remain on our balance sheet and cash proceeds received are reported as liabilities, with related interest expense recognized over the life of the related borrowing. In securitization transactions that qualify for sale accounting, we typically have insignificant continuing involvement as an investor. In the case of both whole loan sales and securitizations, and with the exception of certain of our home loans, we also continue to retain servicing rights to our originated loans following transfer. We view servicing as an integral component of the Lending segment, as we believe our servicing function is an important asset because of the connection to the member it affords us throughout the life of the loan. We directly service all of the personal loans that we originate. We act as master servicer for, and rely on sub-servicers to directly service, all of our student loans and GSE conforming home loans. We believe this ongoing relationship with our members enhances the effectiveness of our Financial Services Productivity Loop by increasing member touchpoints and driving new product adoption by existing members.

We rely upon deposits, warehouse financing and our own capital to enable us to continue to expand our origination capabilities. Our ability to utilize deposits held at SoFi Bank to fund our loans has lowered our overall cost of asset-backed financing relative to alternative sources of funding.

Underwriting Process

We have developed an extensive underwriting process across each lending product that is focused on willingness to pay (measured by credit attributes), ability to pay (measured through income verification), and stability (measured by debt service in relation to other loans). A key element of our underwriting process is the ability to facilitate risk-based interest rates that we believe are appropriate for each loan using proprietary risk models through which we project quarterly loan performance, including expected losses and prepayments. The outcome of this process helps us determine a more data-driven, risk-adjusted interest rate that we can offer our members.

Our personal loan and student loan underwriting models consider credit reports, industry credit and bankruptcy prediction models, custom credit assessment models, and debt capacity analysis, as indicated by borrower free cash flow. Our underwriting strategy utilizes an advanced risk model that provides refined risk separation. Home loans originated by SoFi that are agency-conforming loans are subject to credit, debt service, and collateral eligibility established by GSEs. Home loans originated by us that are non-agency loans are subject to our credit criteria, which typically includes a minimum tri-bureau credit score, established credit history requirements, income verification, as well as maximum qualified mortgage limits on debt-to-income service and caps on loan-to-value based on an accredited appraisal. We also leverage our data to provide existing members a streamlined application process through automation. Across our loan products, existing members generally experience a higher approval rate than new members, subject to the existing member being in good standing on their existing products.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Technology Platform Segment

Our Technology Platform segment consists of Galileo, which we acquired in May 2020, and Technisys, which we acquired in March 2022. Galileo is a provider of technology platform services to financial and non-financial institutions. Through Galileo, we provide services through a suite of program, event and authorization application programming interfaces for financial and non-financial institutions. Technisys is a cloud-native digital and core banking platform with financial services customers predominantly in Latin America. Through Technisys, we earn technology product and solutions revenue through sales of software licenses and provision of maintenance and support services related to those software licenses. We also provide additional technology solutions for our customers as their business needs evolve over time, which we refer to as “evolution labs.”

Financial Services Segment

Our suite of financial services products, by nature, provides more daily interactions with our members and is, therefore, differentiated from our lending products, which inherently have less consistent touchpoints with our members. We offer a suite of financial services solutions, the most significant of which are discussed below.

SoFi Checking and Savings

SoFi Checking and Savings provides a digital banking experience. Following the Bank Merger, we began to allow members to convert their cash management accounts into SoFi Checking and Savings accounts held at SoFi Bank. We believe SoFi Checking and Savings accounts held at SoFi Bank are attractive to our members and prospective members because our digital banking platform allows members to spend, save and earn interest and rewards in flexible ways, all within our mobile application.

SoFi Bank has also continued to expand its services. SoFi Money debit cards are issued by a third party bank, which also sponsored access to debit networks for payment transactions, funding transactions and associated settlement of funds under a sponsorship agreement with SoFi Securities. Further, the third party bank provided sponsorship and support for ACH, check, and wire transactions along with associated funds settlement. While we continue to engage the third party bank, in the fourth quarter of 2022, SoFi Bank gained direct access to debit networks and began to perform certain services previously sponsored by the third party bank. SoFi Securities’ agreement with the third party bank provides for receipt by the third party bank of program revenue and transaction fees, and is subject to a minimum monthly card activity fee. The agreement with the third party bank is terminable by SoFi Securities with 120 days prior notice.

Our legacy cash management product utilizes a sweep administrator to sweep funds to and from program banks, as necessary, under a program broker agreement between SoFi Securities and the sweep administrator, as well as program account and program bank agreements with a variety of sweep program banks. Since becoming a bank, a significant portion of remaining cash management account balances are swept to SoFi Bank as a program bank. The program broker agreement provides for one-year terms that automatically renew and is terminable by either party with at least 90 days prior written notice. Historically, the program account agreements and program bank agreements provided for the rate of interest payable on the balances in a member’s cash management account. Effective June 5, 2022, most of our SoFi Money cash management accounts no longer earn interest, as we implemented our plan to build new features only for SoFi Checking and Savings and reduce support of our SoFi Money cash management accounts.

SoFi Invest

SoFi Invest is a mobile-first investment platform offering members access to trading and advisory solutions, such as active investing, robo-advisory and digital assets accounts. Our interactive investing experience fosters engagement by allowing members to view and monitor other investors’ activity on the platform. We view SoFi Invest as an attractive first product for members who may later become deposit account holders or borrow with SoFi.

Our active investing service enables members to buy and sell stocks and exchange-traded funds (“ETFs”), to engage in options trading, to purchase shares in IPOs before they trade on an exchange, to buy and sell fractional shares and to access a retirement savings account. Our robo-advisory service offers managed portfolios of stocks, bonds and ETFs. Our digital assets service allows members to buy and sell select digital assets through third-party custodians. Additionally, we provide introductory brokerage services to our members and have invested heavily to create an appealing mobile investing experience.

With respect to our digital assets trading activities, we do not hold or store members’ digital assets, but instead rely on third-party custodians, and we hold an immaterial amount of digital assets in order to facilitate paying new member bonuses when members initiate their first digital assets trade. We do this for member convenience to facilitate a seamless payment of digital assets.

SoFi Technologies, Inc.

TABLE OF CONTENTS

In connection with our approval as a bank holding company, the Board of Governors of the Federal Reserve (the “Federal Reserve”) determined that the activities of SoFi Digital Assets, LLC in providing members with the ability to buy or sell various digital currencies through SoFi Digital Assets, LLC's omnibus account with a third-party custodian is not a permissible activity under the Bank Holding Company Act and Regulation Y. However, under Section 4 of the Bank Holding Company Act, the Federal Reserve has permitted us to continue our current digital assets related offering for a two-year conformance period from the date we became a bank holding company, with the possibility for three one-year extensions, provided that we do not expand our impermissible activities, except as authorized by the Bank Holding Company Act and Regulation Y, or increase our established risk limits for total customer digital assets maintained in wallets that are accessible online, referred to as “hot wallets”, or held on balance sheet.

SoFi Credit Card

The SoFi Credit Card product is designed to help our members save, invest and pay down debt through a variable rewards program, with higher rewards offerings when redeeming into other SoFi products. Our credit card product features no annual fee and up to 3% cash back rewards with direct deposit setup through SoFi.

Other

Some of the additional financial services solutions offered within our platform include:

•Loan referrals: A service through which we present loan referral leads to our enterprise customers.

•SoFi Relay: A personal finance management product that allows members to track all of their financial accounts in one place and utilize credit score monitoring services. SoFi Relay also provides us with unified intelligence about our members and offers us meaningful insights about what SoFi products may help our members best achieve their financial goals.

•SoFi At Work: A service through which we partner with other enterprises looking for a seamless way to provide financial benefits to their employees, such as student loan payments made on their employees’ behalf.

•Lantern Credit: A financial services marketplace platform developed to help applicants that do not qualify for SoFi products seek alternative products from other providers, as well as to provide a product comparison experience.

•SoFi Protect: A service through which we partner with providers who offer insurance products to help our members protect their assets, including providers across auto, life, cyber, homeowners, property and casualty, and renters insurance products and estate planning.

We believe that the content and features we provide within our mobile application can spur more financial education, which leads to more ways for our members to actively engage in getting their money right and can ultimately demonstrate the effectiveness of our Financial Services Productivity Loop.

CompetitionWe compete at multiple levels, including: (i) competition among other personal loan, student loan, credit card and residential mortgage lenders, (ii) competition for deposits among other banks, some challenger banks and a variety of technology and retail companies, (iii) competition for investment accounts among other introductory brokerage firms and a variety of technology and other companies, (iv) competition for subscribers to financial services content, and (v) competition among other technology platforms for the enterprise services we provide, such as platform-as-a-service through Galileo and cloud-native digital and core banking services through Technisys.

Competition to fund prime loans. The prime lending market is highly fragmented and competitive. We face competition from a diverse landscape of consumer lenders, including other banks, credit unions and specialty finance lenders, as well as alternative technology-enabled lenders.

Competition to acquire deposits. Although we now operate a bank, many other banks are larger, have been in business longer and often have greater brand awareness than us. Some large technology and retail companies have large consumer bases and strong balance sheets, which could enhance their competitive ability.

Competition to acquire investment brokerage accounts. The leading incumbent brokerage firms are larger, have been in business longer and generally have greater brand awareness than us. We also face competition from neo-brokerage platforms

SoFi Technologies, Inc.

TABLE OF CONTENTS

that provide some of the same features as us, such as a mobile brokerage experience, robo-investing, access to digital assets investing, fractional share investing and options trading. In addition, technology and other companies have begun to offer some basic investing features and the ability to buy and sell digital and other assets.

Competition to attract financial services content viewership. There are many sources of financial news in the marketplace, many of which are more established and have a larger subscriber base.

Competition for technology products and solutions. Generally, these arrangements are multi-year contracts, which require us to spend the necessary resources on implementation and interconnecting new clients onto our platform. We face competition from larger institutions that could make investments into an integrated platform-as-a-service solution or to a cloud-native digital and core banking solution, and also undercut our pricing, preventing our current clients from renewing, while also impeding our attempts to acquire new clients.

MarketingOur sales and marketing efforts are designed to drive brand awareness, improve member acquisition efficiency and accelerate our Financial Services Productivity Loop. We attract and retain members through multiple marketing channels, including social media, traditional media such as the press, online affiliations, search engine optimization, search engine marketing, offline partnerships, preapproved direct mailings and television advertising. We continue to optimize our marketing strategy through a focus on our full suite of financial products and iterate on opportunities to accelerate the Financial Services Productivity Loop.

Government Supervision and RegulationWe are subject to extensive and complex supervision and examination by various federal, state and local government authorities designed to, among other things, protect depositors, borrowers and other customers. The following is a summary of certain aspects of the various statutes and regulations applicable to us and our subsidiaries. This summary is not a comprehensive analysis of all applicable laws, and is qualified by reference to the full text of statutes and regulations referenced below, which may be modified or amended from time to time.

As a bank holding company, we are subject to regulation, supervision and examination by the Federal Reserve under the Bank Holding Company Act of 1956, as amended (“BHCA”), and SoFi Bank is subject to regulation, supervision and examination by the Office of the Comptroller of the Currency (the “OCC”).

Bank Holding Company Regulation. The Federal Reserve has the authority, among other things, to order bank holding companies such as the Company to cease and desist from unsafe or unsound banking practices, to assess civil money penalties and to order termination of non-banking activities or termination of ownership and control of a non-banking subsidiary by a bank holding company.

Source of Strength. Under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”), we are required to serve as a source of financial strength for SoFi Bank. This means that we may be required to provide capital or liquidity support to SoFi Bank, even at times when we may not have the resources to provide such support to SoFi Bank.

Acquisitions and Activities. The BHCA prohibits a bank holding company, without prior approval of the Federal Reserve, from acquiring all or substantially all the assets of a bank, acquiring control of a bank, merging or consolidating with another bank holding company, or acquiring direct or indirect ownership or control of any voting shares of another bank or bank holding company if, after such acquisition, the acquiring bank holding company would control more than 5% of any class of the voting shares of such other bank or bank holding company. The BHCA also prohibits a bank holding company from engaging directly or indirectly in activities other than those of banking, managing or controlling banks or furnishing services to its subsidiary banks. However, a bank holding company may engage in and may own shares of companies engaged in activities that the Federal Reserve has determined, by order or regulation, to be so closely related to banking as to be a proper incident thereto.

The Company has elected to be treated as a financial holding company pursuant to Section 4(l) of the BHC Act. As a financial holding company, the Company is authorized to engage in a broader set of financial activities than a bank holding company that has not elected to be treated as a financial holding company, including insurance underwriting and broker-dealer services as well as activities that are jointly determined by the Federal Reserve and the U.S. Treasury to be financial in nature or incidental to such financial activity. Financial holding companies may also engage in activities that are determined by the

SoFi Technologies, Inc.

TABLE OF CONTENTS

Federal Reserve to be complementary to financial activities. “Financial activities” is broadly defined to include not only banking, insurance and securities activities, but also merchant banking and additional activities that the Federal Reserve, in consultation with the Secretary of the Treasury, determines to be financial in nature, incidental to such financial activities, or complementary activities that do not pose a substantial risk to the safety and soundness of depository institutions or the financial system generally.

If a financial holding company or any depository institution subsidiary of a financial holding company fails to remain well capitalized and well managed, the Federal Reserve may impose such limitations on the conduct or activities of the financial holding company as the Federal Reserve determines to be appropriate, and the company and its affiliates may not commence any new activity or acquire control of shares of any company engaged in any activity that is authorized particularly for financial holding companies without first obtaining the approval of the Federal Reserve. The Company must also comply with all applicable Federal Reserve requirements for financial holding companies. If a financial holding company remains out of compliance for 180 days or such longer period as the Federal Reserve permits, the Federal Reserve may require the financial holding company to divest either its insured depository institution or all of its non-banking subsidiaries engaged in activities not permissible for a bank holding company. If an insured depository institution subsidiary of a financial holding company fails to maintain a “satisfactory” or better record of performance under the Community Reinvestment Act, the financial holding company will be prohibited, until the rating is raised to “satisfactory” or better, from engaging in new activities authorized particularly for financial holding companies or acquiring companies engaged in such activities.

Limitations on Acquisitions of Our Common Stock. The Change in Bank Control Act prohibits a person or group of persons acting in concert from acquiring “control” of a bank holding company unless the Federal Reserve has been notified and has not objected to the transaction. Under a rebuttable presumption established by the Federal Reserve, the acquisition by a person or group of persons acting in concert of 10% or more of a class of voting securities of a bank holding company with a class of securities registered under Section 12 of the Exchange Act constitutes the acquisition of control of a bank holding company for purposes of the Change in Bank Control Act. In addition, the BHCA prohibits any company from acquiring control of a bank or bank holding company without first having obtained the approval of the Federal Reserve. Under the BHCA, a company is deemed to control a bank or bank holding company if the company owns, controls or holds with power to vote 25% or more of a class of voting securities of the bank or bank holding company, controls in any manner the election of a majority of directors or trustees of the bank or bank holding company, or the Federal Reserve determines that the company has the power to exercise a controlling influence over the management or policies of the bank or bank holding company. Under a rebuttable presumption of control established by the Federal Reserve, the acquisition of control of more than 5% of a class of voting securities of a bank holding company, together with other factors enumerated by the Federal Reserve, could constitute the acquisition of control of a bank holding company under the BHCA.

Bank Regulation. SoFi Bank is subject to regulation, supervision and examination by the OCC. Additionally, the FDIC has secondary supervisory authority as the insurer of SoFi Bank’s deposits. SoFi Bank is also subject to regulations issued by the CFPB, as enforced by the OCC. Pursuant to the Dodd-Frank Act, the Federal Reserve may directly examine the subsidiaries of the Company, including SoFi Bank. The enforcement powers available to the federal banking regulators include, among other things, the ability to issue cease and desist or removal orders; to terminate insurance of deposits, to assess civil money penalties, to issue directives to increase capital, to place SoFi Bank into receivership, and to initiate injunctive actions against banking organizations and institution-affiliated parties.

Deposit Insurance. Deposit obligations of SoFi Bank are insured by the FDIC’s Deposit Insurance Fund up to $250,000 per depositor. Deposit insurance premiums are based on assets, while taking into account various factors, including certain financial metrics and a bank’s supervisory ratings. The FDIC has the authority to adjust deposit insurance assessment rates at any time. Under the Federal Deposit Insurance Act (“FDIA”), insurance of deposits may be terminated by the FDIC if the FDIC finds that the insured depository institution has engaged in unsafe and unsound practices, is in an unsafe or unsound condition to continue operations or has violated any applicable law, regulation, rule, order or condition imposed by the FDIC. For 2022, the FDIC insurance expense for SoFi Bank was $4.3 million.

Activities and Investments of National Banking Associations. National banking associations must comply with the National Bank Act and the regulations promulgated thereunder by the OCC, which generally limit the activities of national banking associations to those that are deemed to be part of, or incidental to, the “business of banking”. Activities that are part of, or incidental to, the business of banking include taking deposits, borrowing and lending money and discounting or negotiating promissory notes, drafts, bills of exchange, and other evidences of debt. Subsidiaries of national banking associations generally may only engage in activities permissible for the parent national bank.

Acquisitions and Branching. Prior approval from the OCC is required in order for SoFi Bank to acquire another bank or establish a new branch office. Well capitalized and well managed banks may acquire other banks in any state, subject to

SoFi Technologies, Inc.

TABLE OF CONTENTS

certain deposit concentration limits and other conditions, pursuant to the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994, as amended by the Dodd-Frank Act.

Brokered Deposits. The FDIA and FDIC regulations generally limit the ability of an insured depository institution to accept, renew or roll over any brokered deposit unless the institution’s capital category is “well capitalized” or, with the FDIC’s approval, “adequately capitalized.” Depository institutions that have brokered deposits in excess of 10% of total assets are subject to increased FDIC deposit insurance premium assessments; however, for institutions that are “well capitalized” and have a CAMELS composite rating of 1 or 2, reciprocal deposits are deducted from brokered deposits. Section 202 of the Economic Growth, Regulatory Relief, and Consumer Protection Act (the “Economic Growth Act”), which was enacted in 2018, amended the FDIA to exempt a capped amount of reciprocal deposits from treatment as brokered deposits for certain insured depository institutions.

Community Reinvestment Act. The Community Reinvestment Act (“CRA”) requires the OCC to evaluate SoFi Bank’s performance in helping to meet the credit needs of the entire communities it serves, including low and moderate-income neighborhoods, consistent with its safe and sound banking operation. A bank’s performance under the CRA is taken into consideration when evaluating and approving applications for charters, bank mergers, acquisitions, and branch openings. On January 1, 2023, SoFi Bank began operating under a five-year CRA strategic plan which includes measurable goals relating to: (i) Community Development (“CD”) Lending and CD Investments, (ii) CD Contributions, (iii) CD Services, (iv) Small Business Lending, and (v) Retail Services and Products. SoFi Bank’s 2023-2027 CRA performance will be examined based upon the CRA strategic plan’s five measurable goals as defined in the strategic plan and, as a result, the OCC’s standard performance evaluation criteria will not be utilized to evaluate SoFi Bank’s CRA performance throughout the duration of the strategic plan period. The OCC rates a national bank’s compliance with the CRA as “Outstanding”, “Satisfactory”, “Needs to Improve” or “Substantial Noncompliance”. Failure of SoFi Bank to receive at least a “Satisfactory” rating could inhibit SoFi Bank or the Company from undertaking certain activities, including acquisitions of other financial institutions. Golden Pacific Bank, the predecessor to SoFi Bank, received a “Satisfactory” rating as of April 1, 2019.

Lending Restrictions. Federal law limits a bank’s authority to extend credit to directors and executive officers of the bank or its affiliates and persons or companies that own, control or have power to vote more than 10% of any class of securities of a bank or an affiliate of a bank, as well as to entities controlled by such persons. Among other things, extensions of credit to insiders are required to be made on terms that are substantially the same as, and follow credit underwriting procedures that are not less stringent than, those prevailing for comparable transactions with unaffiliated persons. The terms of such extensions of credit may not involve more than the normal risk of repayment or present other unfavorable features and may not exceed certain limitations on the amount of credit extended to such persons, individually and in the aggregate, which limits are based, in part, on the amount of the bank’s capital.

Enhanced Prudential Supervision. SoFi Bank did not have $10 billion or more of consolidated assets as of December 31, 2022, but it is likely that it will in the near future. In addition, the Company had in excess of $10 billion in total consolidated assets as of December 31, 2022. The Dodd-Frank Act and other federal banking laws subject companies with $10 billion or more of consolidated assets to additional regulatory requirements. Section 1075 of the Dodd-Frank Act, which is commonly known as the “Durbin Amendment”, amended the Electronic Fund Transfer Act to restrict the amount of interchange fees that may be charged and prohibit network exclusivity for debit card transactions. SoFi Bank will be required to comply with the restrictions on interchange fees by July 1, 2023, which may negatively impact future interchange fees.

In addition, Section 619 of the Dodd-Frank Act, commonly known as the “Volcker Rule”, which generally prohibits banking entities from engaging in proprietary trading and from acquiring or retaining an ownership interest in or sponsoring certain types of investment funds, does not apply to an insured depository institution if it, and every company that controls it, has total consolidated assets of $10 billion or less and consolidated trading assets and liabilities that are 5% or less of consolidated assets. While SoFi Bank had total consolidated assets of less than $10 billion as of December 31, 2022, the Company, which controls SoFi Bank, had total consolidated assets in excess of $10 billion as of December 31, 2022. As a result, the Company and SoFi Bank are subject to the Volcker Rule. The Volcker Rule does not significantly impact the operations of the Company and SoFi Bank, as we do not have any significant engagement in the businesses prohibited by the Volcker Rule.

Finally, Section 1025 of the Dodd-Frank Act and the CFPB’s interpretations thereof provide that the CFPB has authority to examine any insured depository institution with total assets of more than $10 billion for four consecutive quarters and any affiliate thereof.

SoFi Technologies, Inc.

TABLE OF CONTENTS

Capital Adequacy and Safety and Soundness

Regulatory Capital Requirements. The Federal Reserve and the OCC have issued substantially similar risk-based and leverage capital rules applicable to U.S. banking organizations such as the Company and SoFi Bank. These rules are intended to reflect the relationship between the banking organization’s capital and the degree of risk associated with its operations based on transactions recorded on-balance sheet as well as off-balance sheet items. The Federal Reserve and the OCC may from time to time require that a banking organization maintain capital above the minimum levels discussed below, due to the banking organization’s financial condition or actual or anticipated growth.

The capital adequacy rules define qualifying capital instruments and specify minimum amounts of capital as a percentage of assets that banking organizations are required to maintain. Common equity Tier 1 capital generally includes common stock and related surplus, retained earnings and, in certain cases and subject to certain limitations, minority interests in consolidated subsidiaries, less goodwill, other non-qualifying intangible assets and certain other deductions. Tier 1 capital for banks and bank holding companies generally consists of the sum of common equity Tier 1 capital, non-cumulative perpetual preferred stock, and related surplus and, in certain cases and subject to limitations, minority interests in consolidated subsidiaries that do not qualify as common equity Tier 1 capital, less certain deductions. Tier 2 capital generally consists of hybrid capital instruments, perpetual debt and mandatory convertible debt securities, cumulative perpetual preferred stock, term subordinated debt and intermediate-term preferred stock, and, subject to limitations, allowances for loan losses. The sum of Tier 1 and Tier 2 capital less certain required deductions represents qualifying total risk-based capital.

Under the capital rules, risk-based capital ratios are calculated by dividing common equity Tier 1 capital, Tier 1 capital, and total capital, respectively, by risk-weighted assets. Assets and off-balance sheet credit equivalents are assigned to one of several categories of risk weights based primarily on relative credit risk. The Tier 1 leverage ratio is calculated by dividing Tier 1 capital by average assets, less certain items such as goodwill and intangible assets, as permitted under the capital rules.

Under the Federal Reserve’s rules that are applicable to the Company and the OCC’s capital rules applicable to SoFi Bank, the Company and SoFi Bank are each required to maintain a minimum common equity Tier 1 capital to risk-weighted assets ratio of at least 4.5%, a minimum Tier 1 capital to risk-weighted assets ratio of 6.0%, a minimum total capital to risk-weighted assets ratio of 8.0% and a minimum leverage ratio requirement of 4.0%. Additionally, these rules require an institution to establish a capital conservation buffer of common equity Tier 1 capital in an amount above the minimum risk-based capital requirements for “adequately capitalized” institutions of more than 2.5% of total risk weighted assets, or face restrictions on the ability to pay dividends, pay discretionary bonuses and to engage in share repurchases.

Under the OCC’s prompt corrective action rules, an OCC supervised institution is considered well capitalized if it: (i) has a total capital to risk-weighted assets ratio of 10.0% or greater, (ii) a Tier 1 capital to risk-weighted assets ratio of 8.0% or greater, (iii) a common Tier 1 equity ratio of 6.5% or greater, (iv) a leverage capital ratio of 5.0% or greater, and (v) is not subject to any written agreement, order, capital directive or prompt corrective action directive to meet and maintain a specific capital level for any capital measure. SoFi Bank is considered well capitalized under all regulatory definitions.

Generally, a bank, upon receiving notice that it is not adequately capitalized (i.e., that it is “undercapitalized”), becomes subject to the prompt corrective action provisions of Section 38 of the FDIA that, for example: (i) restrict payment of capital distributions and management fees, (ii) require that its federal bank regulator monitor the condition of the institution and its efforts to restore its capital, (iii) require submission of a capital restoration plan, (iv) restrict the growth of the institution’s assets, and (v) require prior regulatory approval of certain expansion proposals. A bank that is required to submit a capital restoration plan must concurrently submit a performance guarantee by each company that controls the bank. A bank that is “critically undercapitalized” (i.e., has a ratio of tangible equity to total assets that is equal to or less than 2.0%) will be subject to further restrictions, and generally will be placed in conservatorship or receivership within 90 days.

Current capital rules do not establish standards for determining whether a bank holding company is well capitalized. However, for purposes of processing regulatory applications and notices, the Federal Reserve’s Regulation Y provides that a bank holding company is considered “well capitalized” if: (i) on a consolidated basis, the bank holding company maintains a total risk-based capital ratio of 10.0% or greater, (ii) on a consolidated basis, the bank holding company maintains a Tier 1 risk-based capital ratio of 6.0% or greater, and (iii) the bank holding company is not subject to any written agreement, order, capital directive, or prompt corrective action directive issued by the Federal Reserve to meet and maintain a specific capital level for any capital measure.

Safety and Soundness Standard. Guidelines adopted by the federal bank regulatory agencies pursuant to the FDIA establish general standards relating to internal controls and information systems, internal audit systems, loan documentation, credit underwriting, interest rate exposure, asset growth, asset quality, earnings, and compensation and benefits. In general,

SoFi Technologies, Inc.

TABLE OF CONTENTS

these guidelines require, among other things, appropriate systems and practices to identify and manage the risk and exposures specified in the guidelines. The guidelines prohibit excessive compensation as an unsafe and unsound practice and describe compensation as excessive when the amounts paid are unreasonable or disproportionate to the services performed by an executive officer, employee, director or principal shareholder. In addition, the federal banking agencies adopted regulations that authorize, but do not require, an agency to order an institution that has been given notice by an agency that it is not satisfying any of such safety and soundness standards to submit a compliance plan. If, after being so notified, an institution fails to submit an acceptable compliance plan or fails in any material respect to implement an acceptable compliance plan, the agency must issue an order restricting asset growth, requiring an institution to increase its ratio of tangible equity to assets or directing action to correct the deficiency and may issue an order other actions of the types to which an undercapitalized institution is subject under the “prompt corrective action” provisions of the FDIA. See “Regulatory Capital Requirements” above. If an institution fails to comply with such an order, the agency may seek to enforce such order in judicial proceedings and to impose civil money penalties.

Dividend Restrictions

The Company is a legal entity separate and distinct from its subsidiaries. The right of the Company, and consequently the right of shareholders of the Company, to participate in any distribution of the assets or earnings of its subsidiaries through the payment of dividends or otherwise is subject to the prior claims of creditors of the subsidiaries, including, with respect to SoFi Bank, depositors of SoFi Bank, except to the extent that certain claims of the Company in a creditor capacity may be recognized.

Restrictions on Bank Holding Company Dividends. The Federal Reserve has the authority to prohibit bank holding companies from paying dividends if such payment is deemed to be an unsafe or unsound practice. The Federal Reserve has indicated generally that it may be an unsafe or unsound practice for bank holding companies to pay dividends on regulatory capital instruments unless the bank holding company’s net income over the preceding year is sufficient to fund the dividends and the expected rate of earnings retention is consistent with the organization’s capital needs, asset quality and overall financial condition. In addition, under Federal Reserve policy, the Company should inform the Federal Reserve reasonably in advance of declaring or paying a dividend on regulatory capital instruments that exceeds earnings for the period for which the dividend is being paid or that could result in a material adverse change to the Company’s capital structure. Further, under the Federal Reserve’s capital rules, the Company’s ability to pay dividends is restricted if it does not maintain capital above the capital conservation buffer. See “Capital Adequacy and Safety and Soundness—Regulatory Capital Requirements” above.

Restrictions on Bank Dividends. The OCC has the authority to use its enforcement powers to prohibit a bank from paying dividends if, in its opinion, the payment of dividends would constitute an unsafe or unsound practice. Federal law also prohibits the payment of dividends by a bank that will result in the bank failing to meet its applicable capital requirements on a pro forma basis. In addition, under the National Bank Act, SoFi Bank generally may, without prior approval of the OCC, declare a dividend so long as the total amount of all dividends (common and preferred), including the proposed dividend, in the current year do not exceed net income for the current year to date plus retained net income for the prior two years.

Certain Transactions by Bank Holding Companies with their Affiliates

There are various statutory restrictions on the extent to which bank holding companies and their non-bank subsidiaries may borrow, obtain credit from or otherwise engage in “covered transactions” with their insured depository institution subsidiaries. An insured depository institution (and its subsidiaries) may not lend money to, or engage in covered transactions with, its non-depository institution affiliates if the aggregate amount of covered transactions outstanding involving the bank, plus the proposed transaction exceeds the following limits: (i) in the case of any one such affiliate, the aggregate amount of covered transactions of the insured depository institution and its subsidiaries cannot exceed 10% of the capital stock and surplus of the insured depository institution, and (ii) in the case of all affiliates, the aggregate amount of covered transactions of the insured depository institution and its subsidiaries cannot exceed 20% of the capital stock and surplus of the insured depository institution. For this purpose, “covered transactions” are defined by statute to include a loan or extension of credit to an affiliate; a purchase of or investment in securities issued by an affiliate; a purchase of assets from an affiliate unless exempted by the Federal Reserve; the acceptance of securities issued by an affiliate as collateral for a loan or extension of credit to any person or company; the issuance of a guarantee, acceptance or letter of credit on behalf of an affiliate; securities borrowing or lending transactions with an affiliate that creates a credit exposure to such affiliate; or a derivatives transaction with an affiliate that creates a credit exposure to such affiliate. Covered transactions are also subject to certain collateral security requirements. Covered transactions as well as other types of transactions between a bank and a bank holding company must be conducted under terms and conditions, including credit standards, which are at least as favorable to the bank as prevailing market terms. Moreover, Section 106 of the Bank Holding Company Act Amendments of 1970 provides that, to further competition, a bank

SoFi Technologies, Inc.

TABLE OF CONTENTS

holding company and its subsidiaries are prohibited from engaging in certain tying arrangements in connection with any extension of credit, lease or sale of property of any kind, or the furnishing of any service.

Consumer Financial Services Laws and Regulations

We are subject to federal and state laws designed to protect consumers and prohibit unfair or deceptive business practices. These laws and regulations mandate certain disclosure requirements and regulate the manner in which financial institutions must interact with customers when taking deposits, making loans, collecting loans and providing other services. The CFPB also has a broad mandate to prohibit unfair, deceptive or abusive acts and practices, which can be referred to as “UDAAP”, and is specifically empowered to require certain disclosures to consumers and draft model disclosure forms. Failure to comply with consumer protection laws and regulations can subject financial institutions to enforcement actions, fines and other penalties. The OCC examines SoFi Bank for compliance with CFPB rules and enforces CFPB rules with respect to SoFi Bank. As noted above, the CFPB has authority to examine any insured depository institution with total assets of more than $10 billion and any affiliate thereof.

Truth in Lending Act. The Truth in Lending Act (“TILA”) and Regulation Z, which implements it, require lenders to provide consumers with uniform, understandable information concerning certain terms and conditions of their loan and credit transactions prior to the consummation of a credit transaction and, in the case of certain education, mortgage, and open-end loans, at the time of a loan solicitation, application, approval and origination of a credit transaction. TILA also regulates the advertising of credit and gives borrowers, among other things, certain rights regarding updated disclosures and periodic statements, security interests taken to secure the credit, the right to rescind certain loan transactions, a right to an investigation and resolution of billing errors, and the treatment of credit balances. For certain types of credit transactions, lenders are not permitted to originate loans with certain high-risk features, such as negative amortization and balloon payments, and must provide certain consumer protections during the underwriting and origination process, such as providing a right to an appraisal of mortgaged property, and verifying the consumer’s ability to repay the loan prior to making a decision to approve an application for the loan. Private education lenders must provide multiple disclosures to applicants under TILA and must provide applicants with 30 days in which to accept or reject a loan offer as well as the right to rescind the loan transaction for three business days following receipt of the Final TILA disclosure.

Real Estate Settlement Procedures Act. The federal Real Estate Settlement Procedures Act (“RESPA”) and Regulation X, which implements it, require certain disclosures to be made to the borrower at application, as to the lender’s initial disclosures (or good faith estimate) of loan origination costs, and at closing with respect to the real estate settlement statement; apply to certain loan servicing practices including escrow accounts, member complaints, servicing transfers, lender-placed insurance, error resolution and loss mitigation. RESPA also prohibits giving or accepting any fee, kickback or a thing of value for the referral of real estate settlement services, and giving or accepting any portion of any fee charged for rendering a real estate settlement service other than for services actually performed. To the extent that a lender makes or receives a referral to a third-party with whom it has an affiliated business arrangement, for settlement services, RESPA requires a disclosure to the customer of the affiliation to the service provider. For most home loans, the time of application (loan estimate) and time of loan closing disclosure requirements for RESPA and TILA have been combined into integrated disclosures under the TILA-RESPA Integrated Disclosure rule.

Equal Credit Opportunity Act. The federal Equal Credit Opportunity Act (“ECOA”) prohibits creditors from discriminating against credit applicants on the basis of race, color, sex, age, religion, national origin, marital status, the fact that all or part of the applicant’s income derives from any public assistance program or the fact that the applicant has in good faith exercised any right under the federal Consumer Credit Protection Act or any applicable state law. Regulation B, which implements ECOA, restricts creditors from requesting certain types of information from loan applicants and from using advertising or making statements that would discourage on a prohibited basis a reasonable person from making or pursuing an application. ECOA also requires creditors to provide consumers and certain small businesses with timely responses to applications for credit, including notices of adverse action taken on credit applications.

Fair Housing Act. The federal Fair Housing Act (“FHA”) applies to credit related to housing and prohibits discrimination on the basis of race or color, national origin, religion, sex, familial status and handicap. The FHA prohibits discrimination in advertising regarding the sale or rental of a dwelling, which includes mortgage credit discrimination. The FHA may place restrictions on a creditor’s targeted marketing strategies, due to the risk that such strategies may increase a creditor’s fair lending risk.

Home Mortgage Disclosure Act. The federal Home Mortgage Disclosure Act (“HMDA”) requires lenders to collect, report and disclose certain information about their mortgage lending activity to the CFPB. Much of the data reported pursuant to HMDA is made public and can be used by regulators and third parties to ascertain information about our mortgage lending activity. Regulators and litigants may use the data to make inferences about our compliance with ECOA, FHA and similar anti-

SoFi Technologies, Inc.

TABLE OF CONTENTS

discrimination laws. Effective in 2018, the CFPB issued a final rule which greatly expanded the amount of data that mortgage lenders are required to collect and report under HMDA.

Secure and Fair Enforcement for Mortgage Licensing Act. We employ and contract with mortgage loan originators which are required by state and federal law to be licensed as mortgage loan originators in the relevant jurisdictions where they operate. To obtain and maintain licensure, the mortgage loan originator must meet the minimum education, experience and character requirements set forth by the relevant state’s law, and periodically renew their licenses. We may not be permitted to employ, take applications from, or originate loans processed by mortgage loan originators who fail to maintain a license in good standing in each relevant jurisdiction.

Fair Credit Reporting Act. The federal Fair Credit Reporting Act (“FCRA”), as amended by the Fair and Accurate Credit Transactions Act, promotes the accuracy, fairness and privacy of information in the files of consumer reporting agencies. FCRA requires a permissible purpose to obtain a consumer credit report and requires persons that furnish loan payment information to credit bureaus to report such information accurately. We are also required to perform a reasonable investigation in the event we receive indirect disputes from the credit bureaus about the accuracy of our credit reporting for a particular consumer and to update any inaccurate information we discover. FCRA also imposes disclosure requirements on creditors who take adverse action on credit applications based on information contained in a consumer report or received from a third party and requires creditors who use consumer reports in establishing loan terms to provide risk-based pricing or credit score notices to affected consumers. FCRA also imposes rules and disclosure requirements on creditors’ use of consumer reports for marketing purposes, which impacts our ability to use consumer reports and prescreened lists to market consumer loans through direct mail and other means.

Fair Debt Collection Practices Act. The federal Fair Debt Collection Practices Act (“FDCPA”) provides guidelines and limitations on the conduct of third-party debt collectors in connection with the collection of consumer debts. The FDCPA limits certain communications with third parties, imposes notice and debt validation requirements, and prohibits threatening, harassing or abusive conduct in the course of debt collection. While the FDCPA applies to third-party debt collectors, debt collection and loan servicing laws of certain states impose similar requirements on creditors who collect their own debts or contract with third parties to collect their debts. In addition, the CFPB prohibits UDAAP in debt collection, including first-party debt collection. The CFPB’s Regulation F, which implements the FDCPA, addresses communications in connection with debt collection, interprets and applies prohibitions on harassment or abuse, false or misleading representations, and unfair practices in debt collection, and clarifies requirements for certain consumer-facing debt collection disclosures.

Servicemembers Civil Relief Act. The federal Servicemembers Civil Relief Act (“SCRA”) allows military members to suspend or postpone certain civil obligations so that the military member can devote his or her full attention to military duties. The SCRA requires us to adjust the interest rate of borrowers who qualify for and request relief. The SCRA also places limitations on remedies that may otherwise be available to a creditor, such as foreclosures and default judgments.

Military Lending Act. The Military Lending Act (“MLA”) restricts, among other things, the interest rate and other terms that can be offered to active military personnel and their dependents. The MLA caps the interest rate that may be offered to a covered borrower for most types of consumer credit to a 36% military annual percentage rate, or “MAPR”, which includes certain fees such as application fees, participation fees and fees for add-on products. The MLA also requires certain disclosures and prohibits certain terms, such as mandatory arbitration if a dispute arises concerning the consumer credit product.

Electronic Fund Transfer Act and NACHA Rules. The federal Electronic Fund Transfer Act (“EFTA”), and Regulation E that implements it, provide guidelines and restrictions on the provision of electronic fund transfer services to consumers, and on making an electronic transfer of funds from consumers’ bank accounts. In addition, transfers performed by electronic transfers using the Automated Clearinghouse network (“ACH”) are subject to detailed timing and notification rules and guidelines administered by the National Automated Clearinghouse Association (“NACHA”). Most transfers of funds in connection with the origination and repayment of loans are performed by electronic fund transfers, such as ACH transfers. We obtain necessary electronic authorization from borrowers and investors for such transfers in compliance with such rules. EFTA requires that lenders make available loan payment methods other than automatic preauthorized electronic fund transfers, and prohibits lenders from conditioning the approval of a loan transaction on the borrower’s agreement to repay the loan through automatic fund transfers. Recently, the NACHA Board of Directors approved a change in the NACHA Operating Rules that requires ACH Originators to perform account validation as part of their commercially reasonable fraudulent transaction detection systems.

Electronic Signatures in Global and National Commerce Act/Uniform Electronic Transactions Act. The federal Electronic Signatures in Global and National Commerce Act (“ESIGN”), and similar state laws, particularly the Uniform Electronic Transactions Act (“UETA”), authorize the creation of legally binding and enforceable agreements utilizing electronic records and signatures. ESIGN and UETA require businesses that want to use electronic records or signatures in consumer

SoFi Technologies, Inc.

TABLE OF CONTENTS

transactions and to provide electronic disclosures and other electronic communications to consumers, to obtain the consumer’s consent to receive information electronically.

Bank Secrecy Act. We have implemented various anti-money laundering policies and procedures to comply with applicable federal anti-money laundering laws, regulations and requirements, such as designating a Bank Secrecy Act (“BSA”) officer, conducting an annual risk assessment, developing internal controls, independent testing, training, and suspicious activity monitoring and reporting. We apply the customer identification and verification program rules pursuant to the USA PATRIOT Act amendments to the BSA and its implementing regulations and screen certain customer information against the list of specially designated nationals and other lists of sanctioned countries, persons, and entities maintained by the Treasury Department’s Office of Foreign Assets Control (“OFAC”). Additionally, SoFi Digital Assets, LLC is registered with and regulated by the Financial Crimes Enforcement Network (“FinCEN”) as a money services business (“MSB”) with respect to its digital assets business activities. As an MSB, we are subject to FinCEN regulations implementing the BSA, which requires MSBs to develop and implement risk-based anti-money laundering programs, report large cash transactions and suspicious activity, and maintain transaction records, among other requirements. Similarly, SoFi Bank is a financial institution under the BSA that is required to implement a risk-based anti-money laundering program, including customer identification procedures, currency transaction reporting, suspicious activity monitoring and reporting and other recordkeeping requirements. In addition, our contracts with financial institution partners and other third parties may contractually require us to maintain an anti-money laundering program.

Office of Foreign Assets Control. The U.S. has imposed economic sanctions that affect transactions with designated foreign countries, nationals and others. These sanctions, which are administered by OFAC, take many different forms. Generally, however, they contain one or more of the following elements: (i) restrictions on trade with or investment in a sanctioned country, including prohibitions against direct or indirect imports from and exports to a sanctioned country and prohibitions on “U.S. persons” engaging in financial or other transactions relating to a sanctioned country or with certain designated persons and entities; (ii) a blocking of assets in which the government or specially designated nationals of the sanctioned country have an interest, by prohibiting transfers of property subject to U.S. jurisdiction (including property in the possession or control of U.S. persons); and (iii) restrictions on transactions with or involving certain persons or entities. Blocked assets (for example, property and bank deposits) cannot be paid out, withdrawn, set off or transferred in any manner without a license from OFAC. Failure to comply with these sanctions could have serious legal and reputational consequences for the Company.

Loan Servicing. With respect to our private education loan business, we are subject to the CFPB’s rule that enables it to supervise certain non-bank student loan servicers that service more than one million borrower accounts. The rule covers servicers of both federal and private education loans and is designed to ensure that bank and non-bank servicers follow the same rules in the student loan servicing market. We are impacted by the rule because we have engaged the Missouri Higher Education Loan Authority (“MOHELA”) to service our private education loans. MOHELA currently services more than one million student loan borrower accounts. In addition, for so long as SoFi Lending Corp. acts as servicer of any of our private education loans, we are subject to certain state licensing requirements applicable to loan servicers even though we have engaged MOHELA to service our private education loans, as we retain master servicing rights. With respect to our broader consumer loan business, we are subject to federal and state laws regulating loan servicers. We are impacted by these rules even though we service loans we originate, and engage third parties like MOHELA to service certain types of loans, because some state laws, such as the California Rosenthal Act, apply to creditors and first party servicers. Some state laws also apply to parties that indirectly service loans through the use of third-party servicer contracts. Additionally, we sell some of the loans we originate to third parties and are therefore subject to laws governing parties that service loans on behalf of another person to whom the debt is owed. We are currently licensed as a loan servicer in several states and may be required to seek additional licenses. If we seek additional licenses, a state may impose fines, restrict our activity in that state, or seek other relief for activity conducted prior to the issuance of a license. For example, in 2019, we entered into a consent order with the Commonwealth of Pennsylvania Department of Banking and Securities, requiring us to pay a civil fine for conducting mortgage servicing activity as a master servicer before we obtained a mortgage servicing license in Pennsylvania.

Other State Lending and Money Transmission Laws. SoFi Lending Corp. will continue to service certain of our loans, and our money transmission activities will continue to be provided by SoFi Digital Assets, LLC. Consequently, in addition to applicable federal laws and regulations governing our operations, our ability to service loans through SoFi Lending Corp. in any particular state, and transmit money to or from any particular state, is subject to that state’s laws, regulations and licensing requirements, which may differ from the laws, regulations and licensing requirements of other states. State laws often include fee limitations and disclosure and other requirements. Many states have adopted lending regulations that prohibit various forms of high-risk or sub-prime lending and place obligations on lenders to substantiate that a member will derive a tangible benefit from the proposed credit transaction and/or have the ability to repay the loan. These laws have required most lenders to devote considerable resources to building and maintaining automated systems to perform loan-by-loan analysis of

SoFi Technologies, Inc.

TABLE OF CONTENTS